Most payment failures don't start with a single bad decision. They start with inertia.

We've seen the same pattern play out again and again: you might have a payment setup that works well enough, so it gets left alone. There's always something louder, more visible, and more urgent to fix. But those small deferrals add up, until what once felt stable starts to limit how your business can grow. That's payment inertia, and it's costing businesses more than most realize.

Every payment operation starts the same way. Early on, simplicity is a strength. A single processor is quick to launch, easy to reason about, and more than capable of supporting early growth. But as volume increases, markets expand, and teams scale, that same simplicity becomes a constraint.

Payment maturity isn't about reacting to failure. It's about recognizing when a setup has been outgrown, and acting before fragility shows up at the worst possible moment.

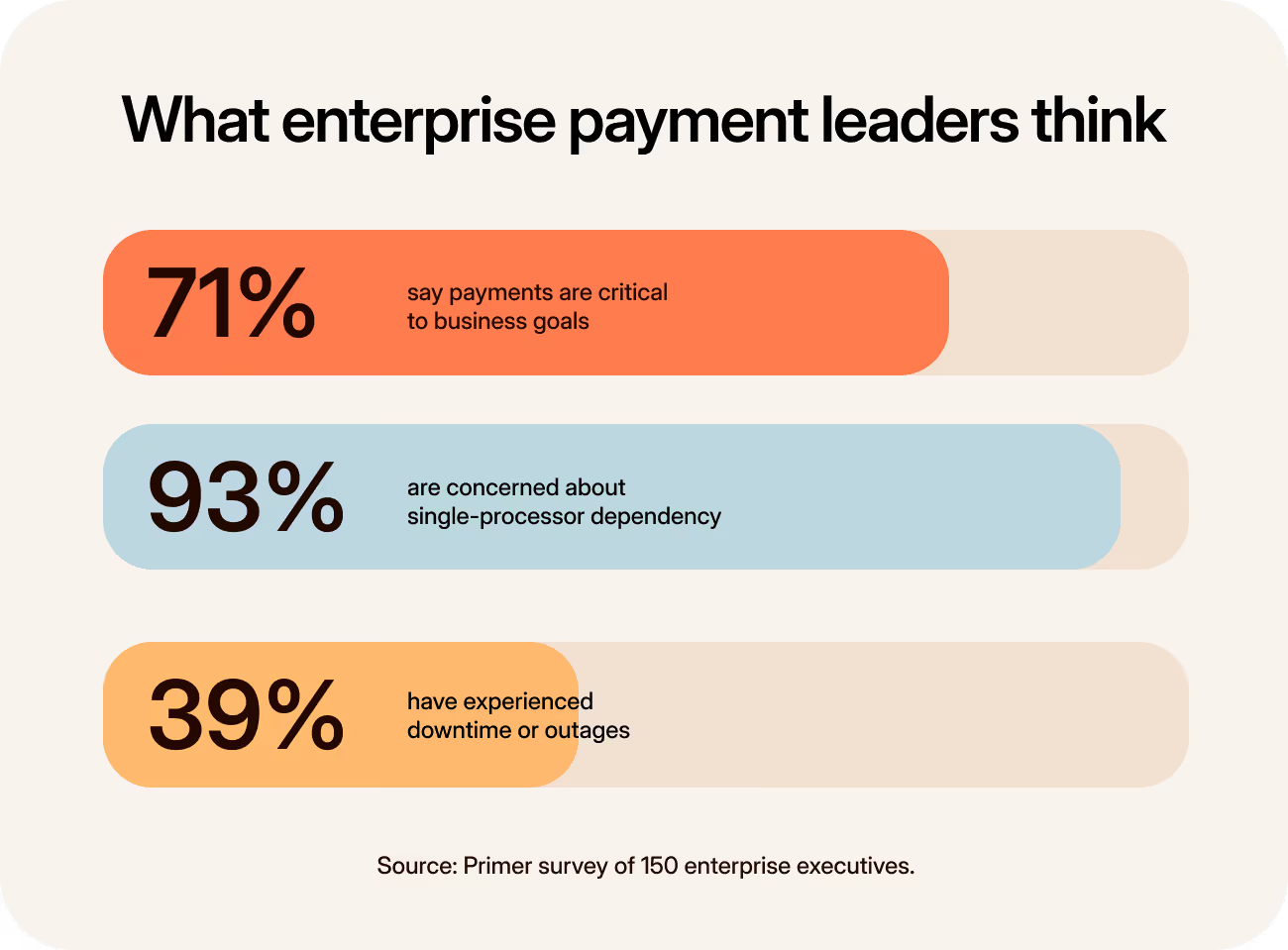

To understand how widespread this problem is, Primer surveyed 150 payment leaders. Here's what they told us

The dependency dilemma

As payments mature, dependency becomes much harder to ignore.

We've spoken to plenty of payment leaders who are confident in the processor they use. The concern isn't that it's unreliable or underperforming. It's that as the business grows, leaving the flow of revenue in the hands of a single platform starts to feel like an unnecessary constraint

That concern is widespread: 93% of payment leaders in our survey say relying on a single processor worries them, with more than half saying they're very concerned. And for good reason. Processor dependency runs deeper than a technical problem. It's a continuity risk, a reputational risk, and a valuation risk rolled into one.

Yet awareness doesn't always lead to action. Even today, we speak to businesses that still rely on one processor. The reasons are familiar: "It's not perfect, but it works." "We'll revisit it next year." Or the one we hear most often: "There are bigger priorities right now."

So dependency remains in place. Not because teams don't understand the risk, but because changing a system that hasn't failed yet is hard to justify. Until, inevitably, it is.

And those failures aren't hypothetical. 39% of payment leaders surveyed have already experienced downtime or outages. When they surface, it's rarely at a quiet moment. They show up under peak load, holiday weekends, major product launches, when systems are most stressed and the margin for error disappears.

The mirage of multiprocessors

The natural response is to introduce more processors.

While the decision is sound—redundancy does reduce exposure and create room to improve performance—this is also where the shape of the stack starts to matter as much as the number of providers involved.

When processors are added without being unified, a different kind of friction appears. Integrations are duplicated, reporting fragments, and teams spend more time coordinating providers than improving outcomes. What looks like progress can quietly become drag.

Redundancy on its own isn’t resilience. Without a unified payments infrastructure to manage and unify these integrations and flows end-to-end, complexity often grows faster than control.

Ferryhopper Chief Product Officer (CPO) and Co-Founder Panagiotis Sarafis puts it well:

“The deeper that we went in payments, the more we found ourselves turning into a payments company rather than focusing on creating the world's best destination to book ferry travel.”

And we see the results play out the same way, time and again:

- Payments teams wait months to make changes, because moving forward first requires unwinding what's already in place.

- Finance teams spend days on manual reconciliation across disconnected systems.

- Product roadmaps slow as engineering capacity is absorbed by yet another PSP integration.

- Fraud and risk teams compensate for gaps across fragmented dashboards

What follows is a payment stack that’s harder to manage, slower to change, and more expensive to maintain than the one it was meant to improve.

Building a payments stack that can evolve

So what does payment maturity, and overcoming inertia, actually look like?

It's neither settling for the status quo nor running a growing collection of processors independently and hoping redundancy alone will absorb the risk. Maturity shows up when payments are designed to evolve alongside the business, rather than being reworked every time something changes.

The difference comes down to having an infrastructure that gives teams the ability to reroute traffic, introduce new providers, test improvements, or expand into new markets without starting from scratch each time.

Ego is a good example of what that looks like in practice. The fashion brand had been outperforming targets, but its success quietly exposed a problem: a PSP contract locked in at lower volumes was generating unnecessary monthly fees, with no leverage to renegotiate. The stack hadn't failed; it had simply been outgrown. With a unified payments infrastructure like Primer, Ego switched to a new PSP in seven days and is now saving €30,000 a month in fees.

Ego's story is one example, but for any business that moves from a fragmented to a unified payments stack, the benefits extend across the whole organization. Finance teams gain a clear view of performance and reconciliation across providers. Payments teams can optimize without waiting on long engineering cycles. Engineers are freed from maintaining fragile integrations and can focus on building products.

That's the shift where payments stop being something the business works around and start becoming something it actively uses to protect revenue, move faster, and support growth.

From inertia to advantage

Processor dependency, hidden inefficiencies, and lack of control are risks most payment leaders are already aware of. Our survey makes this clear. Yet for many, the response is still to wait.

But the cost of staying still compounds quietly in your business, through missed approvals, wasted effort, and fragility that only surfaces under pressure. And because payments sit underneath every critical business outcome, inertia doesn't stay contained. It becomes a constraint on your growth.

You already understand the risk. The challenge is acting on it before the next failure forces the decision.

.png)