As an enterprise business, you're already aware that your payment setup isn't fully optimized. You’re likely processing significant volume through one or two processors. Not because they’re the best option for every transaction, but because adding another processor feels like a project nobody has time for.

You also know that authorization rates vary by region and that local processors often outperform global ones in their home markets. And you know the fees on your current contract could be negotiated down, if you had the data to make the case. But your payments operation is reactive rather than strategic, and the gap between where you are and where you could be is costing you.

Payment orchestration platforms sit between your business and all your payment providers. You integrate once, then manage multiple processors, payment methods, and routing logic from a single layer, with no engineering work required every time something changes. One Primer merchant saved €30k a month and saw a 10% increase in conversion rates within a week of switching. More on that below.

In this article, we cover the specific pain points enterprise payment teams run into, how payment orchestration addresses them, and where Primer’s unified payments infrastructure goes further than standard orchestration.

Primer can help you stop leaving revenue on the table with every payment. Book a call with the Primer team to learn more.

The payment challenges faced by enterprise merchants

For enterprise merchants, the most pressing payment challenge is usually cost, but not just in the way it appears on a processing invoice. At scale, payment costs show up in additional ways that are far harder to quantify, even beyond the standard processing fees.

The specific pressure points tend to be consistent across enterprises:

- Finance teams need to log into multiple PSP dashboards to download reports in incompatible formats, turning reconciliation into a manual, error-prone process that can consume days each month

- Engineering resources are tied up maintaining separate integrations whenever a processor updates its API, pulling developers away from higher-priority work

- Payment operations teams negotiate contracts without reliable data to back them up, leaving them with little leverage to push back on fees

- Cross-border transactions are subject to forced currency conversions, typically adding 1 to 3% on top of processing fees, which can erode margins on every international sale

How payment orchestration reduces costs and complexity for enterprises

Payment orchestration platforms (POPs) consolidate integrations with different payment services into a single tool. You route transactions across payment methods or payment service providers based on custom rules and conditions.

For enterprises that have outgrown a single processor, it removes integration burden and gives payment teams far more flexibility over how transactions are routed and managed. These are the key benefits payment orchestration can offer finance teams.

Activate new PSPs and payment methods quickly

Expanding into a new market typically means months of engineering work, including researching local processors, negotiating contracts, building integrations, and maintaining them as APIs change. For enterprise teams already stretched thin, that timeline often means delaying launches or deprioritizing markets that could be highly profitable.

Adding a new processor or payment method through an orchestration layer takes days instead of months. There’s no separate integration work or lengthy onboarding process, which makes it significantly easier to:

- Test new providers without committing significant engineering resources

- Enter new markets faster

- Build a multi-PSP setup that generates the data needed to negotiate better contracts

Redundancy and resilience

Most enterprises processing through a single processor don't think about downtime until it happens. When it does, every payment fails simultaneously with no warning. For a business processing hundreds of thousands of transactions a month, even a brief outage can mean significant revenue lost in minutes.

With orchestration in place, you can configure automatic fallbacks so that a failed transaction retries through an alternative processor before the customer sees an error. The switch happens in real time behind the scenes.

Smart routing without engineering overhead

When a customer pays, that transaction is sent (or “routed”) to a payment processor that will authorize it. Most enterprises route every transaction to the same processor (like Stripe), regardless of whether it's the most cost-effective or reliable option for that specific transaction type, region, or card issuer.

The result is a one-size-fits-all approach that leaves money on the table and does nothing to recover payments that could have succeeded with a different processor.

Smart routing solves this by letting payment teams define rules that determine where each payment goes based on real transaction data. Rather than hardcoding this logic into your codebase, which requires specialized engineering resources to build and maintain, orchestration lets teams configure routing rules through a dashboard without raising an engineering ticket. In practice, this means being able to:

- Send transactions to processors with optimal fees for specific transaction types

- Implement regional routing strategies, such as sending European transactions to local processors with better authorization rates

- Update routing rules in real time as market conditions change

Where payment orchestration falls short

Payment orchestration was built to solve the routing problem, and at enterprise scale, routing is only one part of what needs to work. Most orchestration platforms don't address key payment challenges, which can create these gaps:

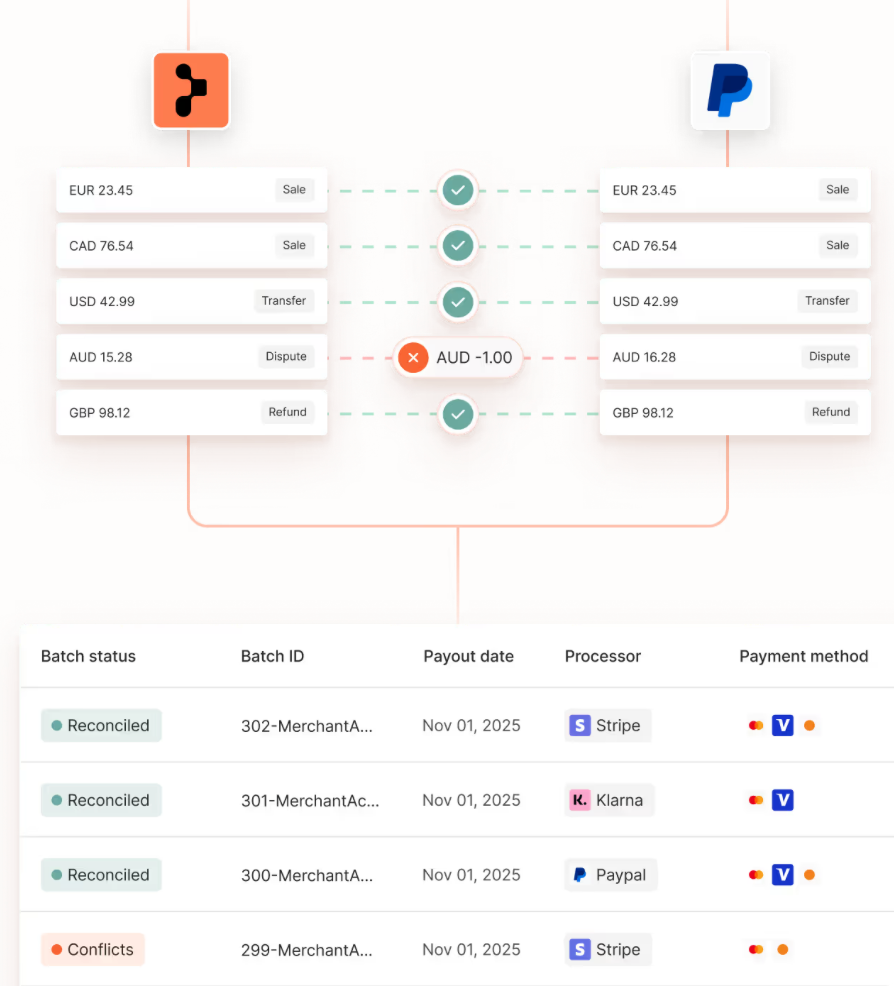

- Reconciliation still requires manual work. Orchestration routes payments but doesn't consolidate reporting. Finance teams still need to log into each PSP dashboard, download reports in different formats, and reconcile them manually. At enterprise scale, this often becomes a job in itself and introduces a higher risk of error.

- FX management remains a separate problem. Orchestration doesn't help a business hold funds in local currencies or reduce cross-border conversion costs. Cross-border transactions still incur FX fees unless another solution is in place.

- Fraud management requires a separate integration. Orchestration platforms don't include fraud tools. That means another vendor, another integration, and another dashboard to manage.

- Negotiating leverage is limited without unified analytics. A multi-PSP setup creates the conditions for negotiation, but without data showing exactly which processors are underperforming, there's no concrete case to make. Processors know that.

- Reporting stays fragmented. Orchestration shows payment flows, but typically doesn't provide the depth of analytics enterprises need to optimize costs across regions, payment methods, and customer segments.

While orchestration is a powerful platform, it doesn’t cover everything. Enterprises typically end up layering additional tools on top: a separate reconciliation platform to consolidate PSP reporting, an FX management tool to handle multi-currency accounts, and a fraud provider with its own integration and dashboard. Each new platform solves one problem and creates another. More vendors to manage, data to reconcile, and fragmentation across the systems your team relies on to make decisions.

This is where Primer's unified payment infrastructure comes in. Rather than stitching together multiple payment platforms, Primer brings routing, reconciliation, FX management, observability, and fraud tool integration together in one place.

How Primer's unified payment infrastructure closes the gap

Most enterprises dealing with payment complexity end up in the same place: an orchestration platform for routing, a separate fraud provider, a reconciliation tool, an FX solution, and reports pulled manually across all of them. Each addition solves one problem but can create another, with more vendors to manage and accounts to reconcile.

Primer is different. As a unified payment infrastructure, it brings routing, payment analysis, reconciliation, global currency management, and fraud tool integration together on one platform. Whether the priority is reducing processing fees, cutting FX charges, streamlining reconciliation, or getting a unified view of payment performance, it's all available without the complexity of managing multiple platforms.

Primer processes billions in volume and is PCI DSS Level 1 certified and SOC 2 compliant, meaning merchants don't need to pursue PCI compliance independently for card data handled through the platform. It's built for scale, with enterprise-grade uptime SLAs.

Why enterprise merchants choose Primer

Primer does everything you'd expect from a payment orchestration platform. Routing logic is configurable through no-code Workflows, new PSPs and payment methods can be activated in days, and Fallbacks protect revenue when a processor goes down.

Here’s where it goes further.

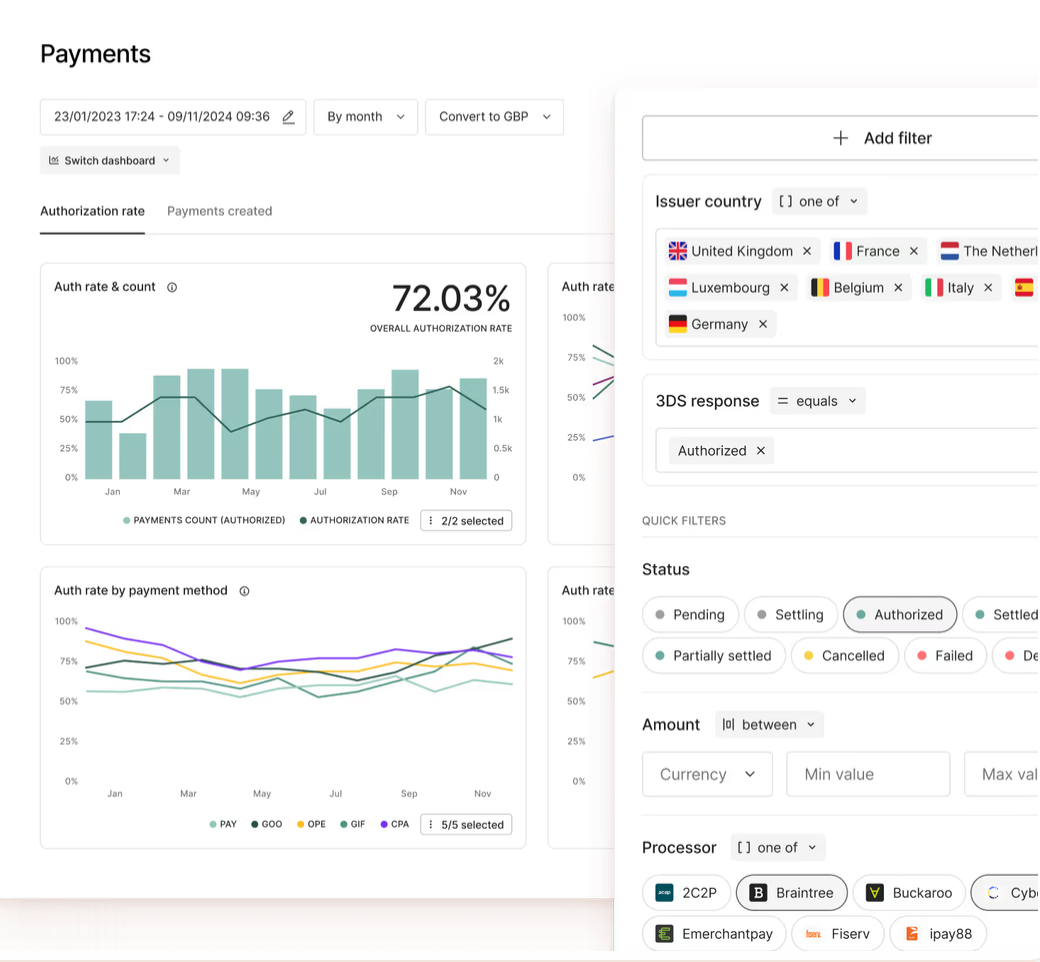

1. Get real-time visibility across your payment stack with Observability

Without a unified view of payment performance, understanding what's happening across your processors means logging into each one individually, downloading data in different formats, and trying to piece it together manually. By the time you have a clear picture, it's already out of date, and any performance issues have had time to compound.

Primer Observability gives payment teams a real-time view across every connected processor, with over 100 visualizations and 30+ filters. Teams can see authorization rates by PSP, region, payment method, and transaction value in a single dashboard, in a consistent format that's easy to track and act on. It’s the kind of clear data that drives more strategic decision making.

It also means payment teams can walk into PSP negotiations with concrete data, showing exactly where a processor is underperforming or where a competitor is delivering better results, rather than relying on the PSP's own reporting.

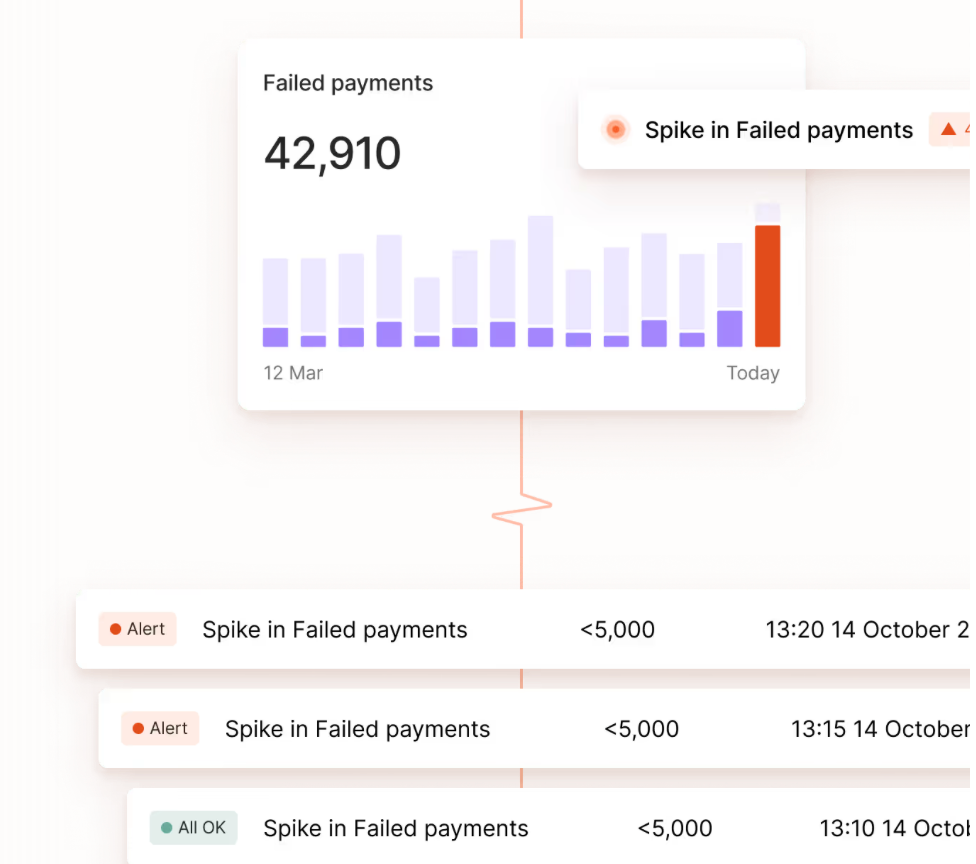

Primer also offers Monitors: automated alerts that trigger when defined thresholds are breached. Drops in authorization rates, spikes in processing costs, or increases in fraud are caught before they compound, not discovered in next month's reconciliation.

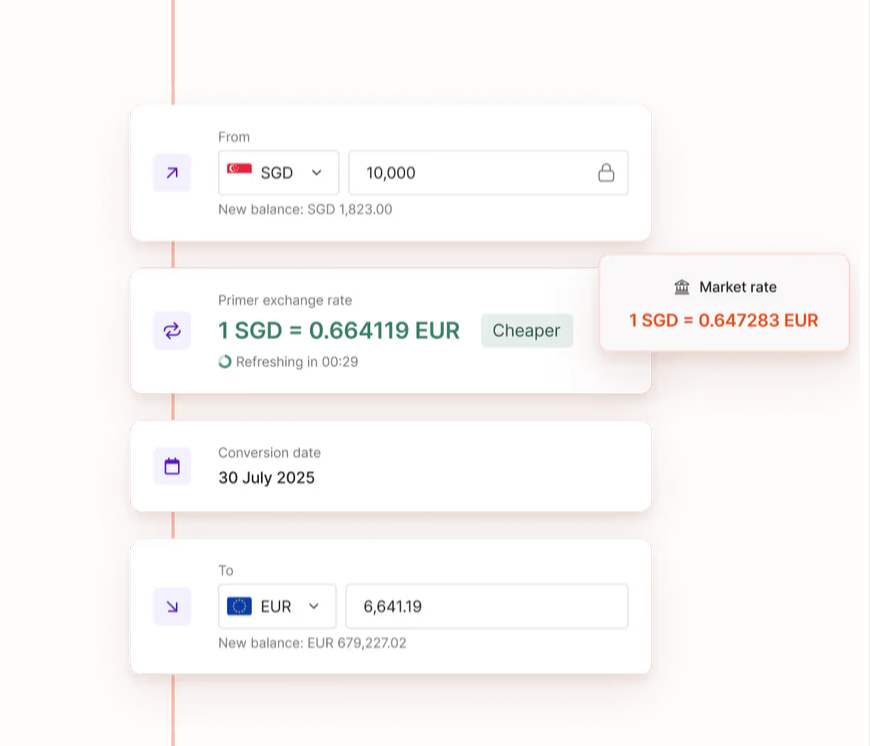

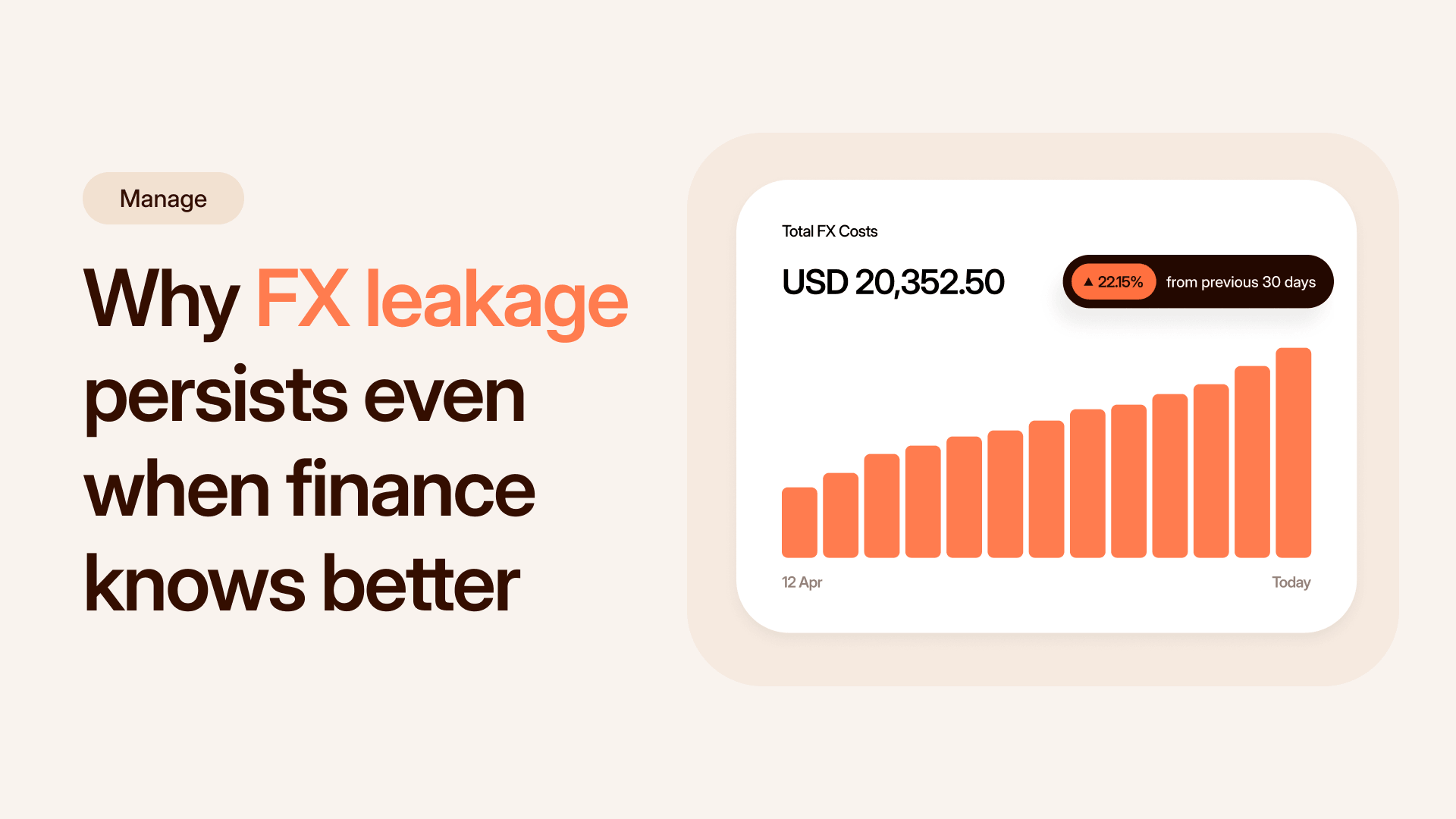

2. Eliminate unnecessary FX costs with Global Accounts

For enterprises processing in multiple currencies, cross-border conversion fees add up quickly. When a business is forced to convert every transaction to its home currency, it pays FX fees on every cross-border payment, and those costs compound at scale.

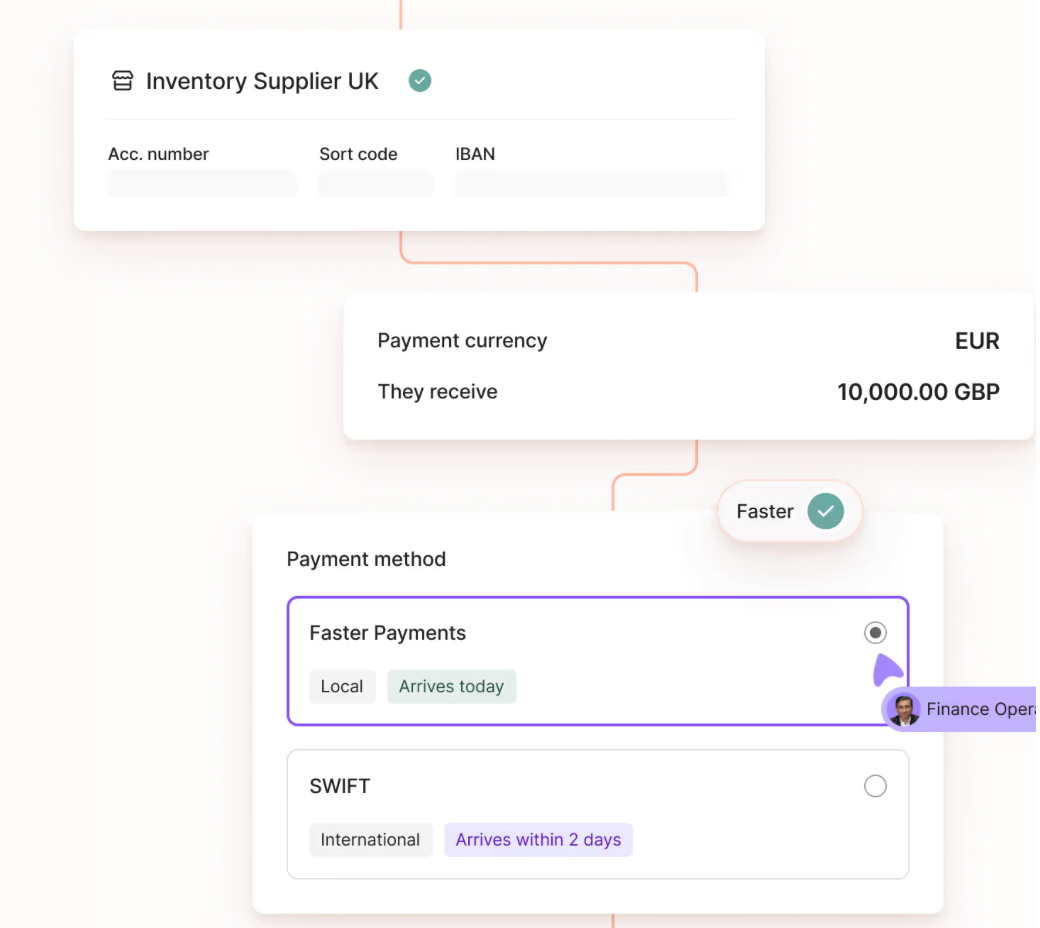

Primer Global Accounts lets you hold, manage, and convert funds in 20+ currencies from a single dashboard. Rather than converting on every transaction, a business can hold funds in local currency, track conversion rates in-platform, and convert when rates are favorable.

You can also ensure you’re using the right PSP in the right area. Pairing local accounts with local PSPs removes cross-border surcharges from the equation entirely, since the transaction no longer crosses currency boundaries.

For enterprises with significant cross-border volume, the FX savings grow with scale.

3. Reduce reconciliation overhead across every processor

Primer Reconciliation pulls transaction data from every connected processor into a standardized format, accessible from a single dashboard. Finance teams work from a single report instead of logging into multiple PSP dashboards and reconciling across incompatible formats.

The time savings are significant and compound monthly, and the reduction in manual handling lowers the risk of errors that are costly to resolve at scale.

How Ego saved €30,000 per month on payment fees with Primer

Ego, a UK fashion retailer, had signed a PSP contract based on projected volume before its mobile app took off. When the app started generating over 30% of revenue, the PSP refused to renegotiate. Ego was locked into fees that penalized its own growth, with no easy way out.

Speed was critical. Using Primer, Ego signed a contract on a Friday and was live with an alternative PSP the following Friday. The switch delivered €30,000 in monthly savings and a 10% increase in conversion rates, an increase the team wasn't even expecting, given how quickly the new checkout had been stood up.

"That's not a marginal gain. It's hundreds of thousands of euros a year that we can reinvest in the company's growth." — Manuel Perez, Head of Software Engineering, Ego

Read the full case study to learn more.

Reduce payment costs and complexity with Primer

Primer is built for enterprise merchants looking to reduce the true cost of payments. This goes beyond processing fees alone, and includes the engineering overhead, reconciliation labor, and FX charges that compound at scale.

One integration connects the full payment lifecycle, from routing and fallbacks through to analytics, reconciliation, and global account management. The cost savings grow as volume does, and is especially valuable if global expansion is your priority.

Book a call to see how Primer can reduce your payment costs and operational overhead.

Frequently asked questions (FAQ): Payment orchestration for enterprise

What’s the difference between payment orchestration and unified payment infrastructure like Primer?

Payment orchestration focuses on routing transactions across multiple PSPs and payment gateways, enabling more flexible payment processing and intelligent routing. Primer goes further by connecting the full payment ecosystem, including reconciliation, payment data, fraud prevention, and global account management, into a single end-to-end platform.

How does payment orchestration improve approval rates and lower costs?

Payment orchestration allows merchants to route transactions to the best-performing acquirers based on region, payment method, or issuer. This improves approval rates and success rates, while also reducing costs by avoiding unnecessary fees, optimizing payment routing, and enabling better pricing negotiations with providers.

Can payment orchestration support global payments and local payment methods?

Yes. Payment orchestration platforms make it easier to scale global payment operations by connecting to local payment methods, alternative payment methods, and regional acquirers through a single integration. This improves the customer payment experience and helps increase conversion in international markets.

How does orchestration impact fraud prevention and authentication?

Orchestration platforms can integrate with fraud detection and fraud prevention tools, allowing merchants to apply rules across their payment systems. This includes managing authentication flows such as 3D Secure, reducing unnecessary friction while maintaining secure payment experiences, and protecting against chargebacks.

Is payment orchestration suitable for high-volume enterprises?

Yes. Payment orchestration is designed for high-volume, enterprise e-commerce businesses that need scalability and automation. It allows teams to manage large transaction volumes, optimize payment strategy in real time, and maintain a seamless payment experience across multiple providers, without increasing operational complexity.

.png)