Europe has never had a single payment method that works everywhere. Merchants selling across France, Germany, Belgium, and the Netherlands have had to integrate separately with each country's local solution, each with its own API, contract, and checkout flow. What if you could offer one pan-European digital wallet that settles funds in seconds?

Wero enables exactly that: pan-European payments. Backed by 30+ banks and financial institutions including BNP Paribas, Deutsche Bank, ING, and Rabobank, Wero is a pan-European digital wallet built on instant account-to-account rails.

It launched for peer-to-peer transfers in mid-2024 and is now rolling out for ecommerce across Germany, Belgium, France, and the Netherlands. By late 2027, it is expected to replace iDEAL entirely.

If you’ve clicked on this article, you’re probably looking for clarity on how seriously to take Wero. That’s exactly what this article is here to help with. We’ll look at where Wero is live, how it fits into the wider European payments landscape, and what its growth could mean for your checkout strategy.

Primer is a unified payment infrastructure that makes it easy to activate new payment methods like Wero without any engineering resources. To see how it works, you can book a demo with Primer.

Everything you need to know about Wero

Wero is a pan-European digital wallet launched by the European Payments Initiative (EPI), a consortium of 16 European banks and financial institutions. It allows customers to pay directly from their bank account using account-to-account (A2A) technology running on SEPA Instant rails. There is no card network, no intermediary, and funds are settled in seconds.

It’s not a new app that customers have to download from scratch. Wero is designed as a layer within existing banking apps, and is already live across Belgium, France, and Germany, with expansion into other European markets underway.

A standalone Wero app is also available on iOS and Android for those who prefer a dedicated interface.

Wero hasn’t launched from zero; it absorbed established national schemes to gain immediate scale. The EPI acquired iDEAL (Netherlands) and Payconiq (Belgium) and migrated Paylib (France) into the Wero platform. This gave it an immediate base of 48 million registered users and over 100 million transactions processed in its first year. This roadmap extends well beyond simple transfers. Wero is building toward one-click checkout, recurring payments and subscriptions, Buy Now Pay Later (BNPL), and in-store payments via NFC and QR code.

Wero is going up against the likes of PayPal, Apple Pay, and the card networks on both functionality and price.

You can learn more about alternative payment methods and how they fit into your broader strategy here: Alternative payment methods: offer customers more ways to pay

How does Wero work?

For your customers, the online payment experience with Wero is frictionless, and takes just a few steps:

- Your customer selects Wero at checkout and gets redirected to their mobile banking app.

- They authorize the payment using their preferred biometric method like Face ID or fingerprint, or by entering their PIN.

- Funds move instantly from their bank account to yours, and they're sent back to your site with the order confirmed.

- The merchant receives real-time confirmation and can fulfill the order immediately.

Authentication is handled by the customer's bank, not a third-party flow. This means strong customer authentication (SCA) compliance is built into the payment process, reducing friction compared to card-based SCA flows. For more on this, take a look at our SCA exemptions guide.

Wero also includes a buyer protection framework for commercial disputes, such as non-delivery or defective goods. This introduces a chargeback-style dispute process to the A2A space.

This is new territory for A2A payments and something merchants need to be aware of operationally: funds can be contested, and the inquiry window is typically 24-72 hours.

Where is Wero available and when is iDEAL migrating?

Wero is already live for peer-to-peer payments in Germany, France, and Belgium, with ecommerce now rolling out across Europe. Germany launched first in late 2025, followed by Belgium and the Netherlands in early 2026, and France and Luxembourg later in the year.

For merchants operating in the Netherlands, the immediate focus is iDEAL.

From late 2026, iDEAL will move fully onto Wero. This is when pricing, contracts, and technical setups are likely to change. By the end of 2027, Wero is expected to fully replace iDEAL.

Wero already has strong bank coverage across Europe, including major players in each market:

- In Belgium: Belfius, BNP Paribas Fortis, ING, and KBC are live.

- In France: BNP Paribas, Crédit Agricole, Crédit Mutuel, Société Générale, LCL, and others.

- In Germany: Deutsche Bank, Sparkasse, Volksbank, Rabobank, ING, and others.

Additional banking groups are joining across all markets through 2026. In-store payments via NFC are coming in 2026, and recurring payments, BNPL, and installment features are also on the roadmap.

As a merchant, this means Wero will become increasingly important as new features roll out. Recurring payments in particular will be critical to get right as you future-proof your payment setup.

The pros and cons of offering Wero for merchants

It goes without saying that if a large portion of your customers want to use Wero, you really ought to be offering it as a payment method.

But what are the implications for you as a merchant? Here are the pros and cons:

How will Primer adapt to Wero when it’s introduced for ecommerce?

As a merchant watching Wero on the horizon, it might feel like yet another payment method to evaluate and another project competing for time, resources, and engineering bandwidth.

You’ve probably been here before: a new APM launches, and suddenly it’s weeks of research, integration builds, testing cycles, and long-term upkeep, all for something that customers increasingly expect to “just work.”

Primer gives you a different path. Instead of stitching together multiple payment methods one by one, you connect once and unlock a unified infrastructure that brings local and global payment options into a single, manageable layer.

So when Wero arrives, you’re not starting from scratch. You’re simply switching it on. No heavy lift, no drawn-out integration, and just a few clicks to activate.

Activate Wero without any code using Primer

Once Wero is live in Primer's connections library, you can activate it in the dashboard instantly with just a few clicks.

You don’t need to integrate anything and there is no ongoing maintenance required from your engineering team.

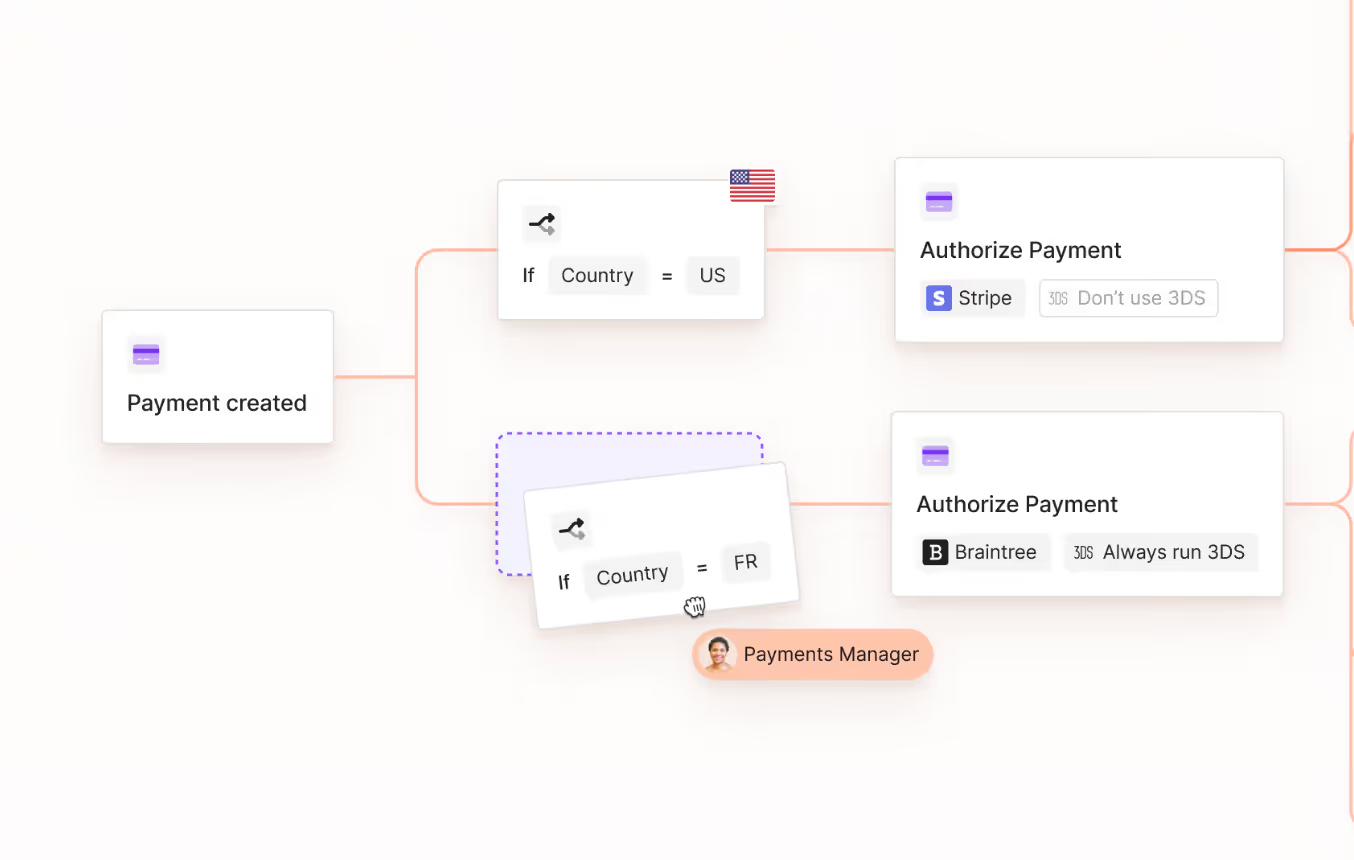

You can then add Wero to Primer Checkout to control when and where Wero appears, such as by country, customer segment, or basket value, all without writing code.

Route and recover Wero payments automatically

Primer Workflows enables you to design smart routing logic for Wero transactions.

For example, you might show Wero to customers in France where bank coverage is strong, while routing card payments through Cartes Bancaires to benefit from lower domestic fees. In Germany, you might prioritize Wero for bank-account payments while keeping local processors available for cards, wallets, or fallback flows.

You can also set up Fallbacks to recover lost revenue in real time. Primer customer Banxa was able to recover US$ 7 million in payment revenue through this one tool.

Analyze Wero performance alongside every other payment method from day one

You can view Wero authorization rates, decline reasons, and conversion by market in Primer Observability alongside every other payment method in your stack.

You get a single source of truth for all your Wero A2A payments alongside your cards and wallets.

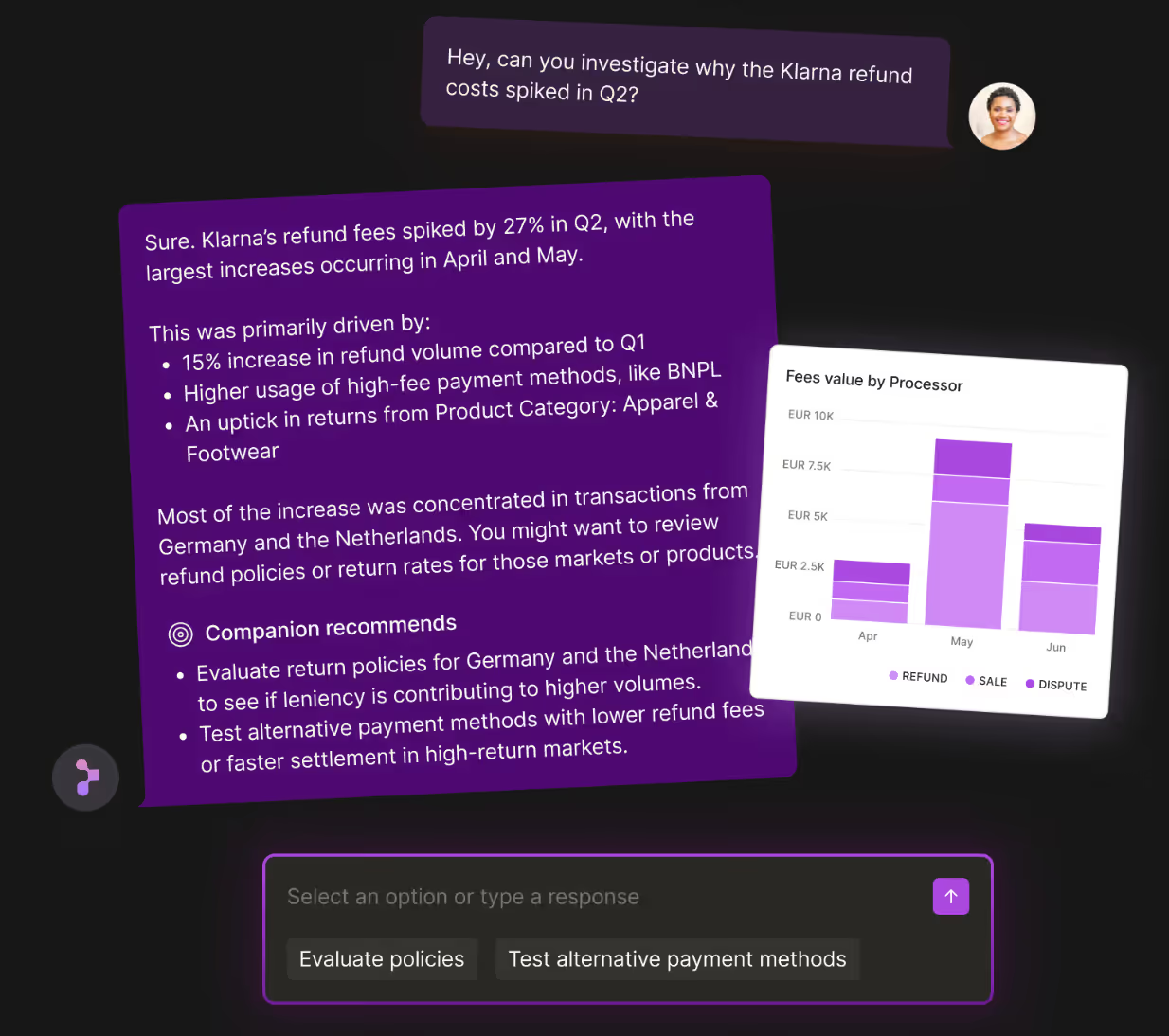

You can also use Primer Companion to help you analyze your performance data every step of the way. It works by surfacing what’s changing across your payment flows, and can recommend optimizations to improve approval rates, reduce your costs, and manage risk.

Read more: How to optimize your checkout: a complete guide

Add Wero to your payment stack without the engineering overhead

Europe's payment landscape has been fragmented for years. Wero is the most significant attempt to change that, offering a single pan-European wallet, backed by the banks that already serve the majority of customers in France, Germany, Belgium, and the Netherlands.

For merchants, the question is not whether to offer Wero. It is how quickly they can do it when it becomes available in their markets and whether their infrastructure makes that a click or a project.

With Primer, it is a click. You activate it, configure it in checkout, set up routing logic, and monitor performance in Observability, all without engineering involvement.

Book a demo to see how Primer makes it easy to add Wero and every other payment method your customers expect.

Frequently Asked Questions: Wero payment method

What is Wero and who is behind it?

Wero is a digital payment solution and pan-European wallet built on instant bank transfer (A2A) technology. It was launched by the European Payments Initiative (EPI), a consortium of major banks including BNP Paribas, Deutsche Bank, ING, and Société Générale.

Unlike traditional card-based payment providers like Visa and Mastercard, Wero enables direct account-to-account payments without intermediaries.

Which European countries is Wero available in?

Wero is rolling out across key European countries, starting with Germany, Belgium, France, and the Netherlands.

It first launched for peer-to-peer payments and is now expanding into ecommerce payment use cases, with broader coverage expected across Europe by 2027.

How does Wero work as a payment solution?

Wero is an instant payments system that allows customers to pay directly from their bank account via their mobile banking app.

At checkout:

- The customer selects Wero

- Confirms the payment in their banking app (often via biometrics)

- Funds are transferred instantly

This mobile payment flow removes the need for cards, reduces friction, and provides real-time confirmation for merchants.

How does Wero compare to card networks like Visa and Mastercard?

Wero differs significantly from traditional payment service providers and card schemes:

- No card rails (unlike Visa or Mastercard)

- No interchange fees

- Faster settlement via instant bank transfers

It represents a shift in the European payments ecosystem toward account-to-account infrastructure rather than card-based processing.

Is Wero replacing existing payment providers like iDEAL and Payconiq?

Yes, Wero is consolidating multiple local payment providers into a single solution:

- iDEAL (Netherlands)

- Payconiq (Belgium)

- Paylib (France)

By 2027, Wero is expected to fully replace iDEAL, creating a unified cross-border payments experience across Europe.

What are the main use cases for Wero?

Wero supports a growing range of use cases, including:

- Ecommerce payments (online checkout)

- Peer-to-peer transfers using a phone number

- Recurring payments and subscriptions (planned)

- In-store point-of-sale (POS) payments via NFC or QR codes (planned)

This makes it relevant across both online and offline digital payment journeys.

Can Wero be used for cross-border payments?

Yes. One of Wero’s biggest advantages is enabling seamless cross-border payments across participating European markets.

Instead of integrating multiple local payment solutions, merchants can offer a single method that works across countries.

How does Wero fit into the wider fintech ecosystem?

Wero is a major development in European fintech, aiming to unify fragmented payment methods into a single, bank-backed system.

It sits alongside other players like Worldline, PayPal, and card networks, but differentiates itself through direct bank integration and instant settlement.

Will Wero support in-store and POS payments?

Yes. Wero is expanding beyond online payments into point-of-sale (POS) environments.

Future capabilities include:

- NFC-based mobile payments

- QR code payments in-store

This will allow Wero to compete directly with in-store solutions currently dominated by cards and wallets.

Do merchants need a new payment service provider to accept Wero?

Not necessarily. Merchants can access Wero through existing payment service providers or unified infrastructure platforms like Primer.

This avoids adding another standalone integration and helps manage multiple payment providers within one system.

How does Wero impact merchant partnerships and payment strategy?

Wero is backed by strong partnerships between major European banks, which gives it significant distribution from day one.

For merchants, this means:

- Access to millions of existing banking app users

- Reduced reliance on card networks

- A more streamlined European payment ecosystem

.png)

.avif)