What happens when your payment processor goes down?

If you're relying on a single acquirer, the answer is your entire business goes offline.

That's not the only risk. If they hike their fees, you pay. If you expand to a new region and approval rates tank, you're stuck. And if you want to switch? You're looking at a months-long engineering project just to add a second processor.

Single-acquirer dependency is a single point of failure, and gives you zero negotiating leverage.

Multi-acquirer routing fixes this. By connecting to two or more processors and directing traffic based on real-time data, you can optimize for cost, speed, and approval rates, without being held hostage by any one provider.

The catch is that setting it up without a payment orchestration platform can require a lot of engineering resources.

This guide covers what a multi-acquirer strategy actually looks like, and how to implement it without a multi-month engineering project.

Note: learn how Primer can help you with multi-acquirer routing by booking a demo with one of our payment experts.

What is multi-acquirer routing?

At its core, multi-acquirer routing simply means using more than one payment processor and then choosing the best one for each transaction.

Instead of sending every payment through a single provider, you might send it through the provider that:

- Has the highest chance to approve the payment

- Costs the least

- Is more reliable for that customer’s region

This is often referred to as smart routing, where transactions are automatically directed based on predefined rules like location, card type, or value.

This enables you to make strategic payment routing decisions to increase approval rates, reduce costs, and create a more reliable payment experience without manual intervention.

For example, you might generally use Stripe for global payments, but route European transactions to a different acquirer, like Adyen, to reduce processing fees.

Read more: A guide to payment routing: Everything you need to know

Three reasons multi-acquirer routing is essential

Every size of business ought to set up multi-acquirer routing, whether that’s for simple redundancy or for optimizing costs as your volume grows.

Here are three reasons to set up multi-acquirer routing:

1. Build redundancy and protect revenue with automated fallbacks

Processor outages are rare but they happen. And for merchants in high-risk industries like gaming, there's an even more immediate threat: getting offboarded with little to no warning when an acquirer decides you no longer fit their risk appetite.

Both scenarios have the same outcome: your payments stop and revenue drops to zero.

A back up processor, known as a fallback, prevents this.

When an issue is detected, whether it's a technical outage or a sudden loss of processing capability, traffic is automatically rerouted to a secondary provider before customers even notice.

For example, imagine a gaming operator running on a single acquirer. A policy change triggers offboarding. Without a backup, deposits fail instantly. With an automated fallback strategy in place, traffic shifts to another processor in real time and players keep depositing so revenue keeps flowing.

2. Use regional price differences to lower your processing fees

Processor fees are negotiable, but only if you have a credible alternative, and a single-acquirer setup gives you none.

Multi-acquirer routing gives you access to a wider pool of processors, and with that comes the ability to send each transaction through whichever acquirer offers the lowest fees for that specific route. A global processor will typically apply cross-border markups as standard, regardless of whether a cheaper local option exists.

For example, a domestic transaction in Germany processed through a local acquirer will often carry lower fees than the same transaction routed through a global processor.

This strengthens your position when it comes to negotiations. When processors know you can shift volume elsewhere, the dynamic changes. You are no longer a captive customer accepting whatever pricing model is put in front of you. You are a merchant with real alternatives, which gives you a much stronger position to push for better rates, reduced minimums, or more favourable contract terms.

Without that flexibility, your options are limited. You can push back on pricing, but without the ability to actually move volume, processors have little reason to budge. The result is higher fees, less room to optimize, and no leverage for negotiations.

3. Route based on performance to lift authorization rates

No processor performs equally well in every market. One acquirer might have deep ties with issuing banks in the UK, while another excels in Southeast Asia due to local licenses, stronger data coverage, or more sophisticated routing logic. If you're sending all transactions through a single processor, you're accepting whatever approval rate they can deliver, regardless of whether a better option exists.

Smart routing lets you take advantage of these differences. Instead of defaulting to one acquirer, you direct each payment to the processor most likely to approve it, based on factors like Bank Identification Number (BIN), issuing bank, card type, and geography.

For example, a UK-issued card might see higher approval rates through a local acquirer with direct issuing bank connections, while a card from Singapore could perform better through a regional specialist with stronger coverage in that market. The transaction is the same, but the outcome changes depending on where you send it.

Over time, even small gains in authorization rates translate into meaningful revenue uplift, particularly at scale. A one or two percentage point improvement across millions of transactions can make a huge difference to your bottom line.

How to set up multi-acquirer routing without payment orchestration

Many merchants attempt to build multi-processor payment routing in-house, only to discover that the engineering overhead is overwhelming.

Here’s what’s involved:

- Choose and onboard multiple processors: You'll have to research, negotiate, and complete "know your customer" (KYC) processes for every new PSP. This is a non-negotiable part of the process.

- Build each integration independently: Every processor has its own API structure, authentication methods, and error handling. Integration can take four to eight weeks per processor, and you'll face ongoing maintenance costs every time a PSP updates its documentation.

- Write custom routing logic: You have to build the code that decides which processor handles which transaction. This logic lives in your codebase and must be manually updated every time you want to test a new rule or change a fee threshold.

- Standardize decline codes: Each PSP uses different return codes for failure reasons. Your engineering team essentially needs to learn a new language, by decoding decline codes to know when it’s safe to retry and when retrying would result in a scheme fine.

- Manage 3D Secure (3DS) across stacks: Most 3DS solutions are processor-native, which means they tie authentication to that specific environment. If a payment fails with Processor A and retries with Processor B, the 3DS result usually won't transfer. The customer is forced to authenticate again, leading to high drop-off rates.

Most merchants who go the DIY route stop at two processors because the cost of adding a third is simply too high.

While negotiating with acquirers is a non-negotiable part of the process, steps 2 to 5 don’t need to be. Solutions like Primer completely eliminate the engineering side of adding new acquirers.

How to set up multi-acquirer routing with Primer

Primer is a unified payment infrastructure that connects you to a library of local and global processors through a single integration.

Instead of building everything yourself, you get a single integration that connects you to multiple processors. You can set up multi-acquirer payment routing without rebuilding your payments stack.

What normally takes months can be done in hours.

Here’s how it works:

Step 1. Activate your processors

Navigate to the connections library in the Primer dashboard. Once your commercial agreement is in place with a PSP, activating it in Primer is a matter of clicks. There is no custom API work because we’ve already built and maintained the integrations for you.

Step 2. Set up smart routing with Workflows

Using drag-and-drop Workflows, you can set up dynamic payment routing rules without writing a single line of code. You can set conditions based on any data point, such as routing to a local acquirer or using a specific global processor for transactions above a certain value.

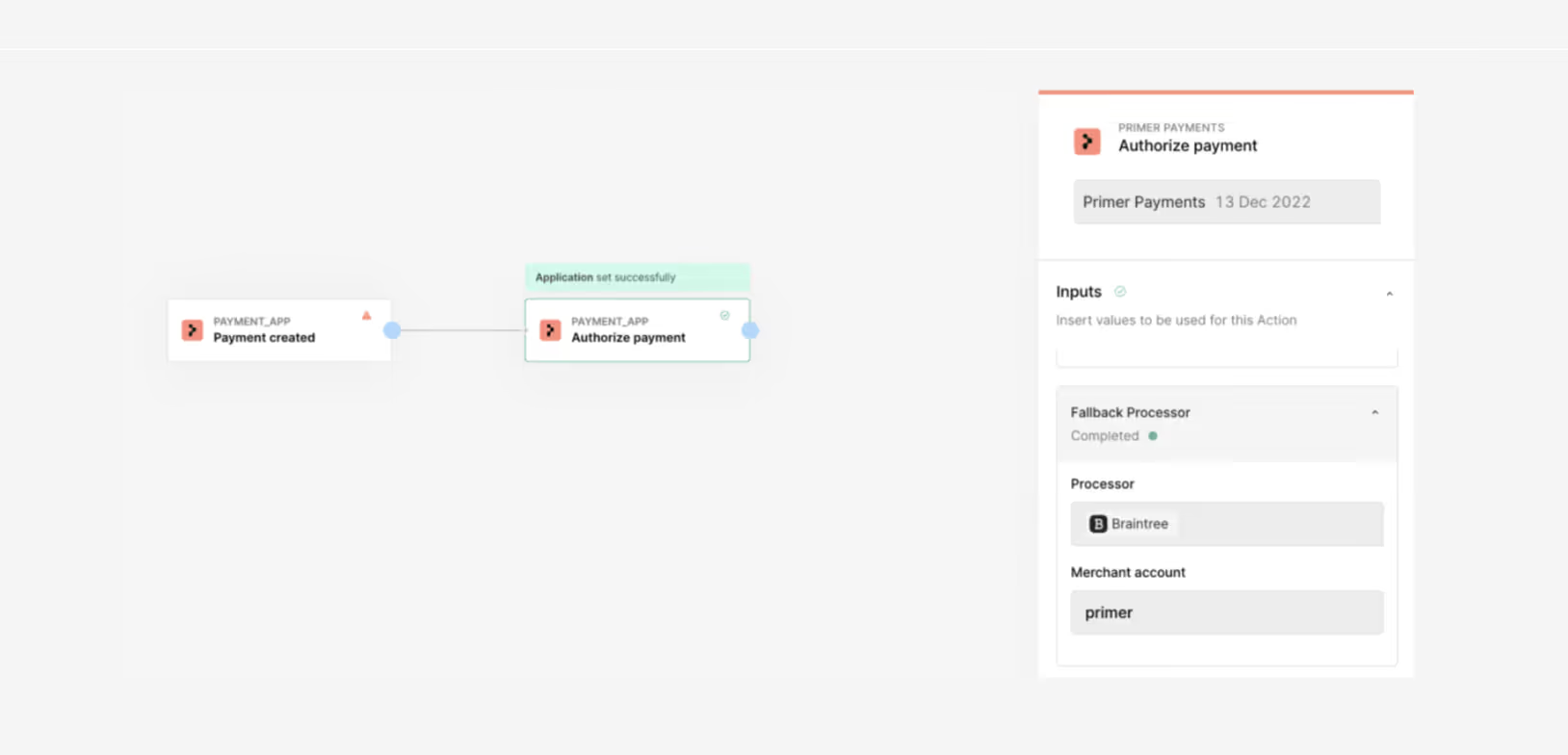

Step 3. Configure Fallbacks and Primer 3DS

Enable Fallbacks to recover failed payments in real time. Primer will only retry when there is a soft declined payment (meaning it’s recoverable).

Because Primer 3DS is agnostic and sits above the processor layer, authentication happens once, and the result passes to any fallback processor. This eliminates the need for the customer to re-authenticate during a retry flow, reducing the chances of drop-off.

Step 4. Store tokens in Primer’s PCI Level 1 compliant vault

To route returning customers or recurring payments between acquirers, your payment data can’t be locked to a single processor.

Primer stores card tokens in an independent, PCI DSS Level 1 compliant vault. This means payment details aren’t locked into one provider, so you can move transactions freely between acquirers.

This enables you to apply routing rules to every payment, not just first-time checkouts. Subscriptions keep working, returning customers aren’t disrupted, and you’re free to experiment with payment routing to optimize for cost, performance, or reliability without being constrained by your infrastructure.

Read more: Why your business needs a processor-agnostic credit card vault

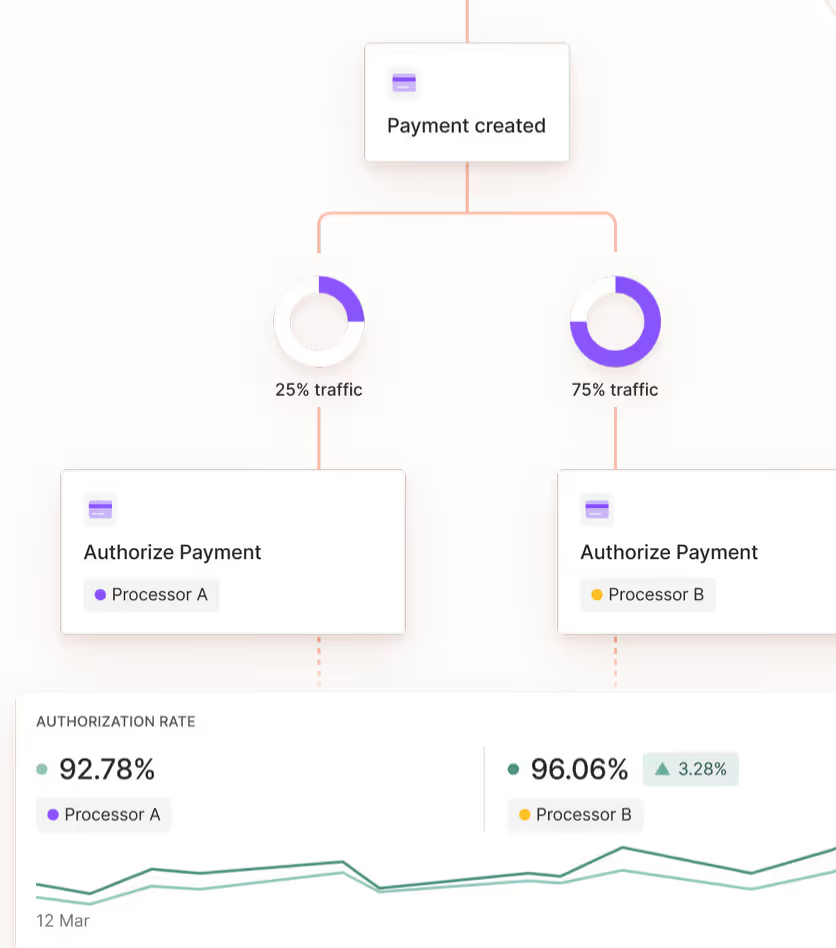

Step 5. Analyze performance in Primer Observability

Multi-acquirer routing isn't a "set it and forget it" task. Primer Observability pulls data from every connected processor into one view. You can compare authorization rates side-by-side or set up Monitors to alert you to a performance drop in a specific region.

Primer Companion, your AI payments analyst within the Primer platform, can also help you make sense of that data as you go. It surfaces what’s changing across your payment flows, explains why it matters, and recommends optimizations to improve approval rates, reduce costs, and manage risk.

How leading merchants are using multi-acquirer routing with Primer

Leading global brands use Primer to optimize their payment strategy, without being bound by engineering constraints. For example:

- Ferryhopper, a fast-growing online travel agency, uses Primer to orchestrate payments across multiple PSPs, markets, and currencies. During peak season, Primer Fallbacks automatically rerouted failed transactions to a secondary processor when a processor issue hit, helping Ferryhopper recover approximately €3.4 million in transactions in a single month. The company also improved its authorization rate from 91.76% to 93.87% year-on-year, even as transaction volume grew by 47%.

- Banxa, a crypto infrastructure provider, operates in a high-risk vertical where processor stability is volatile. Using Primer's Fallbacks, the company recovered $7 million in revenue that would have otherwise been lost to declines.

- Dabble, a fast-growing sports betting platform, achieved a 10%+ increase in global authorization rates. By utilizing multi-acquirer logic and Fallbacks, Dabble recovered over AUD $1,000,000 in revenue in 2025 alone.

Set up multi-acquirer routing without the engineering overhead

Multi-acquirer routing is one of the most direct ways to reduce processing fees and increase resilience, but setting it up without a solution like Primer can be too resource-heavy for many merchants.

Primer removes that barrier. You can activate a range of global and local processors in clicks, build routing logic without code, and recover revenue automatically with agnostic 3DS.

Ready to see how Primer makes multi-acquirer routing work for you? Book a demo with our team.

Frequently asked questions (FAQ)

What is the difference between multi-acquirer routing and payment fallbacks?

Multi-acquirer routing, also known as transaction routing or dynamic routing, is the logic that decides which processor or acquiring bank receives a transaction first. It helps merchants route transactions across multiple acquirers based on cost, performance, geography, or payment type.

Payment fallbacks are the secondary logic that automatically retries or reroutes a failed payment with an alternative processor if the first attempt is declined. This helps reduce declined transactions, improve acceptance rates, and protect the customer experience during checkout.

Do I need to be PCI DSS compliant to do multi-acquirer routing?

Yes, but the level of effort depends on your payment processing infrastructure. If you build routing yourself and handle raw card data across payment service providers, you face a rigorous SAQ-D audit.

If you use Primer, we handle the PCI compliance for you through our agnostic vault and secure tokenization. This makes it easier to manage a multi-acquirer setup without adding unnecessary compliance complexity to your payment flows.

Can multi-acquirer routing help with 3DS friction on payment retries?

Only if your 3DS solution is agnostic. If you use a payment gateway or processor’s built-in 3DS, a retry with a second processor usually requires a second authentication, which can harm the user experience and reduce conversion rates.

Primer solves this by performing 3DS authentication once and passing the result to every fallback attempt. This helps merchants maintain a smoother checkout experience while improving authorization performance across the wider payment ecosystem.

How long does it take to set up multi-acquirer routing with Primer?

Once your commercial contracts and acquiring relationships with processors are signed, activating them in Primer and setting up your first routing Workflow takes hours, not months.

The payment API remains the same regardless of how many acquirers, payment methods, digital wallets, or alternative payment methods you add. This helps ecommerce merchants streamline their payments infrastructure while adding new payment options and payment types over time.

How do I know which routing rules to set up?

Good routing rules are driven by data. Most merchants start by routing based on issuing country or local payment performance, using local acquiring to improve approvals and save on fees.

You can use Primer Observability to compare authorization performance by region, BIN, processor, card network, and payment method. From there, you can refine your logic to send traffic where it performs best, improve conversion rates, reduce downtime, and build a more cost-effective acquiring strategy.

Can multi-acquirer routing improve profitability?

Yes. By routing each transaction to the most suitable acquiring solution, merchants can reduce processing costs, improve approval rates, and recover revenue that would otherwise be lost to failed payments.

A strong routing strategy can also support fraud prevention, manage chargeback risk, improve checkout reliability, and increase overall profitability across ecommerce and digital commerce channels.

.png)

.avif)