Walk into any kopitiam in Kuala Lumpur, and you'll see it: customers tapping their phones to pay for roti canai, hawkers displaying QR codes next to cash registers, even parking meters that accept e-wallets. What was once a cash-dominated society has transformed almost overnight.

Following the pandemic, Malaysia became the second-leading country in Southeast Asia for cashless payment adoption, and alternative payment methods (APM) are quickly becoming the standard.

For merchants looking to expand into Malaysia, this presents both an opportunity and a challenge: how can you make sure you integrate with the right payment methods for this market? And how can you do this without too much engineering overhead?

This guide will aim to help by running you through which payment methods actually matter in Malaysia and a solution that helps you integrate them effortlessly.

Ready to start adding Malaysian payment methods without the engineering lift? Book a call with the Primer team to learn more.

The essential payment methods for Malaysian e-commerce

1. Digital wallets

E-wallet usage has increased quickly over the past few years, with a December 2025 survey finding that 54% of Malaysians have used digital wallets within the three previous months.

GrabPay is one of the most widely adopted wallets in the country, integrated with Grab — Southeast Asia's leading ride-hailing, food delivery, and digital payments platform. That ecosystem gives it a natural distribution across millions of Malaysian consumers who already use Grab daily. Other popular wallets include Touch'n Go, ShopeePay, Boost, and MAE, though availability varies by payment provider.

Why merchants should offer digital wallets

Digital wallets are driven by government incentives, wallet provider promotions, and widespread merchant acceptance. For Malaysian consumers, they reduce checkout friction, especially on mobile, where QR code integration makes them simple to use. Not offering digital wallets in this market means leaving a significant share of transactions on the table.

2. Account-to-account (A2A) payments (FPX, DuitNow)

Built on real-time payment rails, A2A payments enable direct bank transfers and continues to be among the most popular APMs in Malaysia.

Why merchants should offer A2A payments

FPX and DuitNow resonate with Malaysian consumers who prefer the directness and familiarity of bank-based payments. FPX (Financial Process Exchange) is Malaysia's most popular account-to-account payment method.

For higher-value purchases like electronics, furniture, or travel bookings, many Malaysians gravitate toward bank transfers. It feels more secure, more transparent, and more within their control.

The merchant benefits can be significant. Transaction fees are lower than card payments, settlement happens near-instantly, and chargebacks are nonexistent. Because FPX connects to all major Malaysian banks, it reaches virtually the entire banked population without requiring customers to sign up for anything new.

Without FPX and DuitNow in your payment stack, you're potentially losing out on conversions.

3. Buy Now, Pay Later (BNPL)

Buy Now, Pay Later services are experiencing rapid growth in Malaysia. The BNPL payment market currently has over 5 million users, and that number is projected to more than double by 2030.

Atome has built the largest merchant network in Malaysia beyond single-platform ecosystems, partnering with major retailers across fashion, electronics, beauty, and lifestyle categories. Customers can split purchases into three interest-free installments with instant approval at checkout, making it a low-friction option for higher-ticket purchases. Other widely-used BNPL options include SPayLater, embedded within the Shopee app, and Grab PayLater, which benefits from Grab's vast ecosystem across ride-hailing, food delivery, and digital payments, though availability varies by provider.

Why merchants should offer BNPL

BNPL increases average order value by making larger purchases more manageable, reduces cart abandonment on higher-ticket items, and appeals particularly to younger consumers. As adoption accelerates in Malaysia, offering these options can capture sales that might otherwise be lost to upfront cost concerns.

4. Credit and debit cards

Cards payments are table stakes; every merchant will offer them as a baseline payment option. In Malaysia specifically, cards account for approximately 30% of e-commerce payments, which is lower than in many Western markets but still represents a significant portion of transactions.

While digital wallets and FPX are popular domestically, cards remain essential for international customers. Given that 44% of Malaysian e-commerce is cross-border spending, accepting Visa and Mastercard is critical for capturing international shoppers.

Cards also serve as an important backup payment method and are preferred by certain consumer segments, particularly for specific transaction types or higher-value purchases.

How Primer makes it simple to add new payment methods in Malaysia

Primer gives payment teams control of how money moves across their entire business, from adding new payment methods and checkout design, to managing FX and reconciliation.

Instead of building and maintaining separate integrations for Touch'n Go, FPX, Grab Pay, and cards, you connect once to Primer and gain access to everything you need.

Here's how Primer helps merchants scale into Malaysia and beyond.

Add Malaysian payment methods easily

Adding payment methods like GrabPay with Primer takes minutes, not months. Here's how it works:

- Step 1: Integrate once using Primer’s unified API.

- Step 2: Choose your methods from Primer’s list of integrations (Apple Pay, Google Pay, Klarna, iDEAL, PayNow, etc.).

- Step 3: Configure display rules in the Primer Dashboard to show relevant methods by region or device.

- Step 4: Go live: no extra engineering required.

What used to require weeks of engineering effort now takes minutes.

Customize your checkout with Primer Checkout

Primer Checkout lets you configure which payment methods appear at checkout based on customer attributes, region, device type, cart value, and custom logic.

For instance, you can ensure Malaysian shoppers see GrabPay prominently while showing different options to customers in Singapore, Thailand, or international markets.

Checkout is fully customizable, so you can control styling, layout, and UI components, including colors, fonts, spacing, and interactions, using flexible configuration and CSS variables. This means you can create a checkout experience that feels completely aligned with your brand without needing to build or maintain custom frontend code.

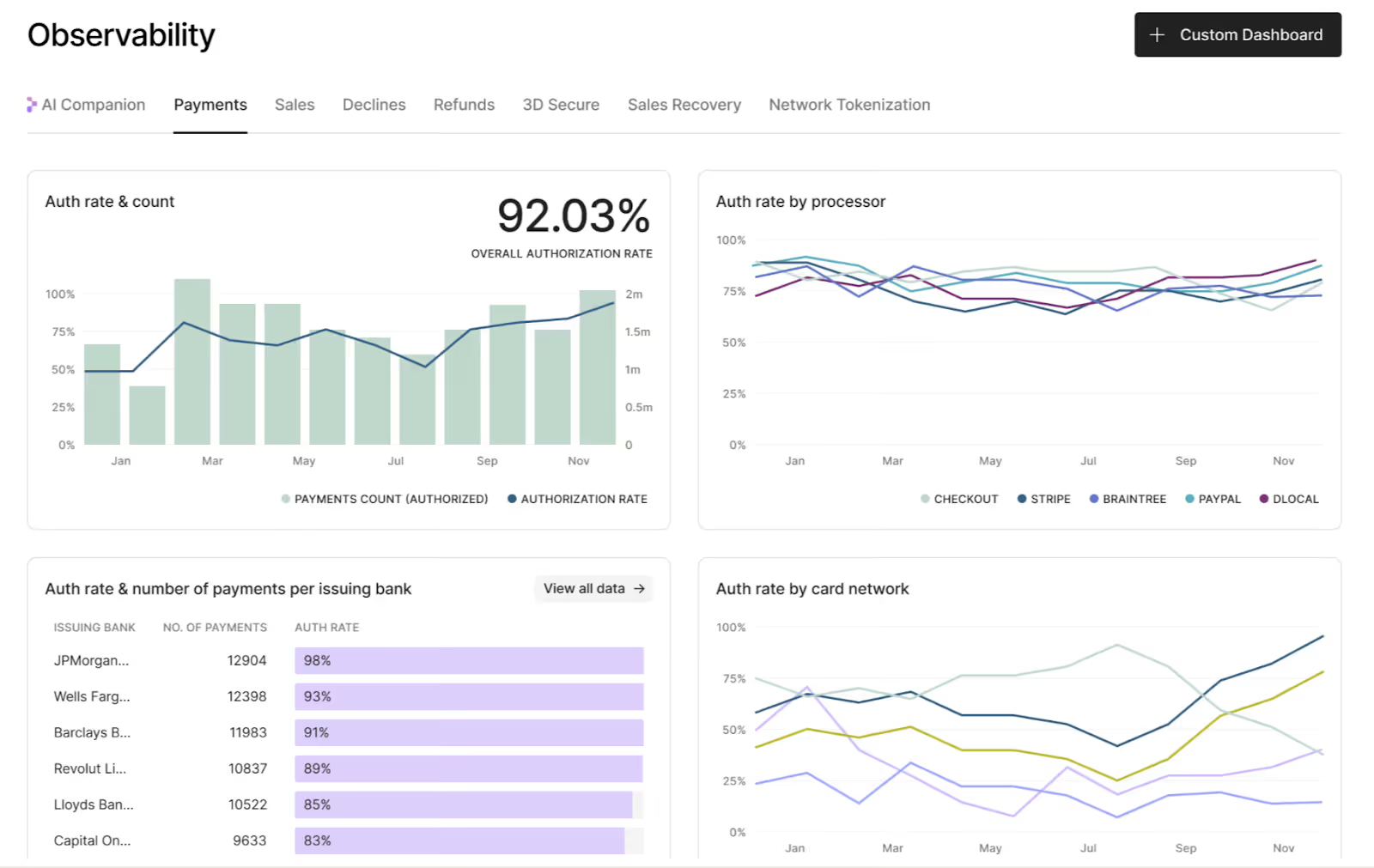

Unify your data with Observability

Primer Observability consolidates data from every processor into a single view. Instead of logging into each provider dashboard separately, each with different metrics and formats, you see everything in one place.

When you're processing hundreds of thousands of payments daily, this visibility is invaluable. You can quickly debug issues, compare authorization rates across processors, and identify where performance is falling short.

Observability also makes A/B testing straightforward. You can compare the performance of two processors in Malaysia by splitting traffic between them, and the data you gather gives you leverage when negotiating contracts and helps you identify where you can save on fees.

With unified data across your entire processor stack, patterns become visible and actionable — helping you continuously optimize performance as you scale in Malaysia and beyond.

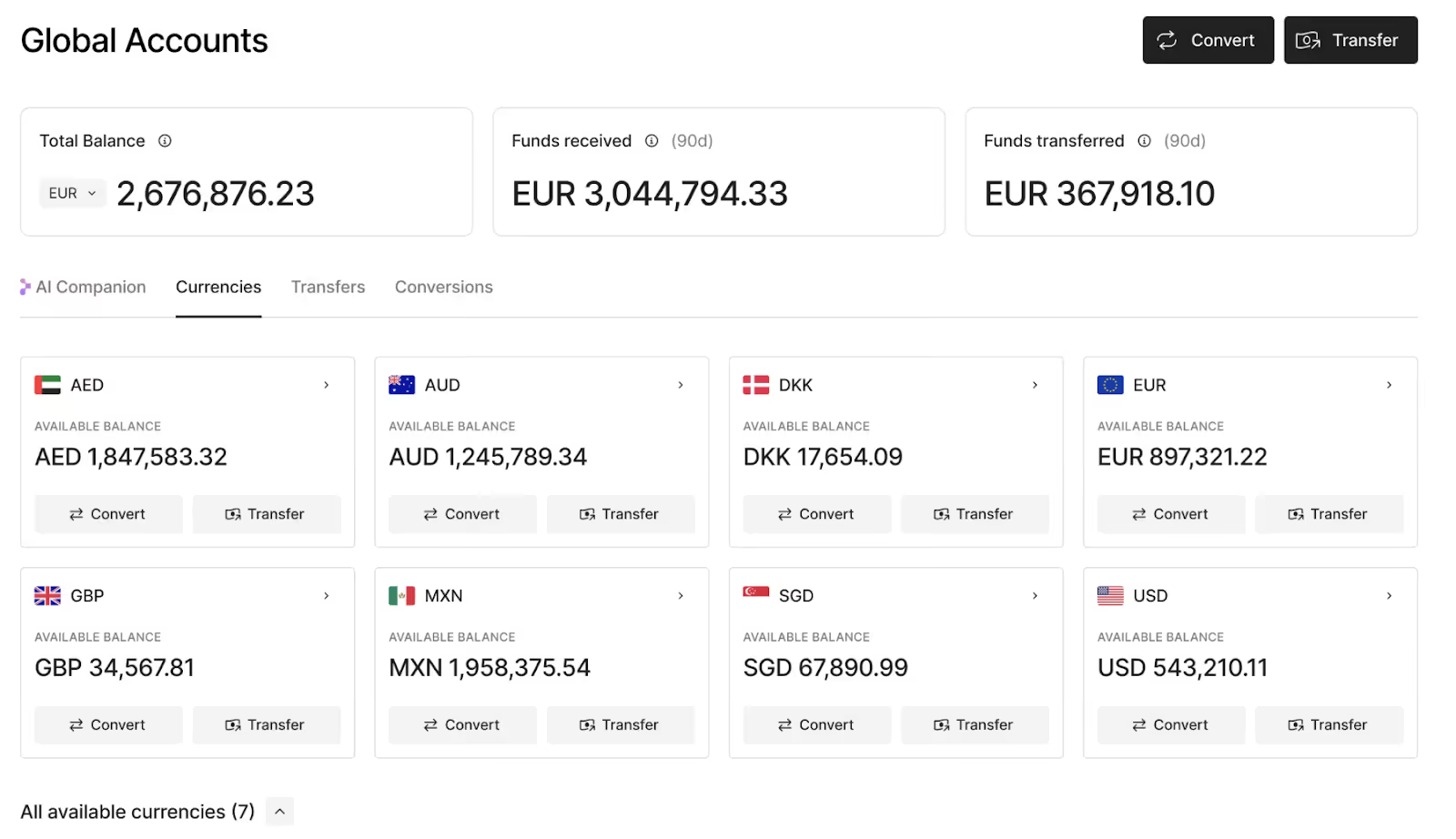

Reduce costs with Global Accounts

Global Accounts lets you open local accounts in 20+ countries and currencies from one place. Instead of being forced to convert currencies through your PSP at opaque rates, you can collect and hold Malaysian ringgit locally, and convert to other currencies on your own terms with transparent, market-linked FX rates.

This reduces cross-border fees—critical when 44% of Malaysian e-commerce is cross-border spending—and simplifies expansion. Once you've established your payment stack for Malaysia, scaling to other Southeast Asian markets becomes significantly easier.

Build your Malaysian payment stack with Primer

Malaysia represents a massive opportunity for merchants willing to meet local payment preferences. The country is transforming rapidly, with most Malaysians favoring cashless options and the government's 2030 cashless goal creating momentum for digital payment methods.

While building and maintaining each integration is doable in-house, it requires a huge amount of engineering resources.

But with Primer, you can add the payment methods Malaysian customers expect, customize your checkout for different segments, and unify your payment data, all without requiring any code.

Book a call to start controlling every transaction end-to-end with Primer.

Frequently asked questions (FAQ)

What are the must-have payment methods for e-commerce in Malaysia?

For most merchants, the baseline payment methods include digital wallets (especially Touch'n Go), FPX (account-to-account payments), BNPL, and cards (Visa/Mastercard). Touch'n Go is used by 90% of Malaysian consumers, making it particularly critical.

The goal isn't to cover the methods Malaysian shoppers expect to see at checkout so you don't lose conversion on payment preference alone.

Why is Touch'n Go so important for Malaysian e-commerce?

Touch'n Go is used by approximately 90% of Malaysian consumers, making it by far the most popular digital wallet in the country. It's become embedded in daily life for Malaysian shoppers, driven by government incentives, merchant adoption, and wallet provider promotions.

For merchants entering Malaysia, Touch'n Go's absence at checkout can directly impact conversion rates because consumers expect to see it as a payment option.

What is FPX and why do Malaysian consumers prefer it?

FPX (Financial Process Exchange) is Malaysia's most popular account-to-account payment method. It enables direct bank transfers built on real-time payment rails. Malaysian consumers trust FPX because funds move directly from their bank account without intermediaries, it offers the security of traditional banking channels, and it's particularly popular for higher-value transactions.

Is Malaysia really going cashless by 2030?

The Malaysian government has set a goal of becoming a cashless society by 2030. While this is an ambitious target, the momentum is significant: 70% of Malaysians favor ditching cash for digital payments, Malaysia became the second-leading country in Southeast Asia for cashless payment adoption following the pandemic, electronic money transactions reached over 100 billion Malaysian ringgit in 2023, and QR code usage jumped from 25% to 61% in just one year. Whether the country fully achieves "cashless" status by 2030, the trend toward digital payments is undeniable.

Do I need multiple PSPs to accept payments in Malaysia?

It depends on which payment methods you want to offer. Some payment methods can be integrated directly (like certain BNPL providers), while others are only available through specific PSPs. To offer the complete payment mix Malaysian customers expect— including Touch'n Go, FPX, Grab Pay, BNPL, and cards—merchants often end up working with multiple PSPs.

Without payment orchestration, this creates operational complexity: multiple integrations, dashboards, contracts, and reporting formats. Unified payment infrastructure platforms like Primer help solve this by allowing merchants to manage multiple PSPs and payment methods through a single integration.

.png)