Every time a customer taps, swipes, or clicks “pay,” a slice of that revenue disappears before it ever lands in your merchant account.

Most merchants know fees are part of the deal. Few, however, can trace where that money actually goes, or explain why two transactions that look identical on the surface can cost different amounts behind the scenes.

That’s because card processing is rarely transparent. Interchange fees, scheme fees, and processor markups are typically rolled into a single blended rate, obscuring the true cost of each payment. This means that margins get chipped away in ways that are hard to spot, let alone control.

Interchange fees make up the largest share of payment costs, yet they’re often the least understood. And that gap in understanding could be costing you revenue. For high-growth businesses, even small improvements in how interchange is managed can translate into meaningful savings at scale.

This guide breaks it down: what interchange fees really are, how they’re calculated, and, most importantly, what finance teams can do to start taking back control over payment costs.

What are interchange fees?

Interchange fees are transaction fees that the merchant’s bank (the acquirer) pays to the customer’s bank (the issuer) every time a card is used for a purchase. While you might see them as a single line item on a summary, interchange is essentially a "transfer fee" between banks to compensate the issuer for the risks of fraud and the costs of managing the cardholder's account.

Most merchants encounter interchange bundled into a total Merchant Discount Rate (MDR). For example, a standard flat fee of 2.9% + $0.30 contains three distinct layers:

- The interchange fee: Paid to the cardholder's issuing bank (usually the largest portion).

- The scheme or assessment fee: Paid directly to the card network (Visa or Mastercard) for using their infrastructure.

- The processor's markup: The margin kept by your payment service provider.

Because interchange typically accounts for 70 to 90% of the total fee, not seeing the breakdown means you could be overpaying without realizing it. These rates are set by the card networks, not your processor. While you can’t negotiate the interchange rate itself with your PSP, you can control how those rates are packaged and which transactions you route to different providers.

Interchange rates vary wildly across different regions. In the US, average credit card interchange ranges from 1.41% to 2.7% for Visa and Mastercard. In contrast, the EU caps these fees at 0.3% for credit cards and 0.2% for debit cards. Card networks typically adjust these rates twice a year, in April and October, making regular review a necessity for cost-sensitive finance teams.

How interchange fees are calculated

Interchange rates are not fixed. They are dynamic, determined by a combination of factors that quantify the risk and "value" of a transaction. If you want to achieve interchange fee optimization, you must understand the variables that trigger higher rates.

The main factors that determine the interchange rate include:

- Card type: Debit cards have lower rates than credit cards. Among credit cards, premium or rewards cards (like a Visa Infinite or corporate card) carry much higher rates because the interchange fee funds the cardholder's rewards program.

- Transaction method: Card-present transactions (swiping or dipping at a terminal) have the lowest rates. Card-not-present (CNP) transactions, like online payments, are considered higher risk and carry a premium.

- Merchant Category Code (MCC): Card networks assign a code based on your industry. Some categories, like utilities or education, may qualify for special lower rates, while travel or high-risk sectors often face higher tiers.

- Geography: Domestic transactions are significantly cheaper than cross-border ones. If you process a UK-issued card through a US based acquirer, you will be hit with cross-border interchange markups.

- Data completeness: For B2B transactions using corporate or government cards, submitting additional "Level 2" or "Level 3" data (like line-item detail or tax information) can significantly reduce the interchange rate.

The cumulative total of these fees, along with network assessments and markups, forms your Merchant Discount Rate. This Merchant Discount Rate represents the full percentage fee deducted from every sale. When these components are bundled, you lose the ability to see if a high Merchant Discount Rate is due to risky transactions or simply an expensive payment instrument type.

Read more: How to reduce card payment fees

Interchange pricing models: what you are actually paying

The way your processor presents interchange costs determines how much control you have over your profit margins. There are three primary models used in the industry today.

1. Flat rate (blended pricing)

This is the model popularized by platforms like Stripe and Square. You pay a single percentage on every transaction (e.g. 2.9% + $0.30), regardless of the actual underlying interchange cost. While simple to budget for, it is rarely optimized.

You effectively pay the same premium on a low-cost domestic debit transaction as you do on an expensive international rewards card, meaning your low-cost transactions are subsidizing the processor's margin.

Best for: Startups or low-volume merchants who prioritize simplicity over margin.

2. Interchange plus (IC+)

In this model, the processor passes the exact interchange fee and scheme fee through to you, adding a fixed markup (e.g. Interchange + 0.3% + $0.10). This is far more transparent. You see exactly what the banks charged and exactly what your processor earned. When card networks lower rates, you see the savings immediately.

Best for: Scaled merchants who want transparency and the ability to optimize costs over time.

3. Tiered pricing

Processors group transactions into "Qualified," "Mid-Qualified," and "Non-Qualified" tiers. They decide the criteria for these tiers, which are often opaque. In practice, many transactions "downgrade" to the highest-cost tiers for reasons that are never clearly disclosed on your statement. This is generally the least favorable model for the merchant.

Best for: Highly specific use cases, but generally avoided by modern finance teams due to hidden costs.

How can you pay less in interchange fees?

Optimization is about changing your transaction behavior to qualify for the best possible rates.

Here’s what’s in your control:

- Switch to an interchange-plus pricing model: You cannot optimize what you cannot see. Moving to IC+ is the prerequisite for any cost-saving initiative, as it reveals the true breakdown of your fees.

- Utilize network tokenization: Replacing raw card data with tokens issued by card schemes improves security. Card networks often reward network tokenization with lower interchange rates because the transaction is deemed lower risk.

- Settle transactions promptly: Card networks expect transactions to be settled within a standard window, typically 24 hours. Delayed settlement can trigger "non-qualified" downgrades, resulting in high-fee penalties.

- Submit Level 2 and Level 3 data: If you are a B2B merchant, ensuring your payment API passes line-item detail and invoice numbers can slash interchange rates on corporate and purchasing cards.

- Consider account-to-account (A2A) methods: Shifting volume away from cards entirely through bank transfers or local payment methods eliminates interchange fees from the equation entirely.

Read more: How to reduce FX fees for global businesses

How Primer helps you manage and reduce payment costs

Primer is a unified infrastructure provider that acts as the control centre for how modern businesses move money.

With a single integration, Primer unlocks a global network of payment processors, giving you the freedom to build, optimize, and scale your payment stack without engineering constraints.

Primer gives you complete visibility into every transaction, every route, every outcome, and the ability to act on it instantly.

One of the major ways Primer can help your bottom line is by optimizing your payment fees.

Here’s how:

See cost and performance across every processor in one place and use that data to negotiate your fees

Interchange is fixed, but processor markup isn’t. The challenge is that most PSPs don’t report fees the same way, which makes it difficult to compare providers properly or understand where margin is leaking across your stack.

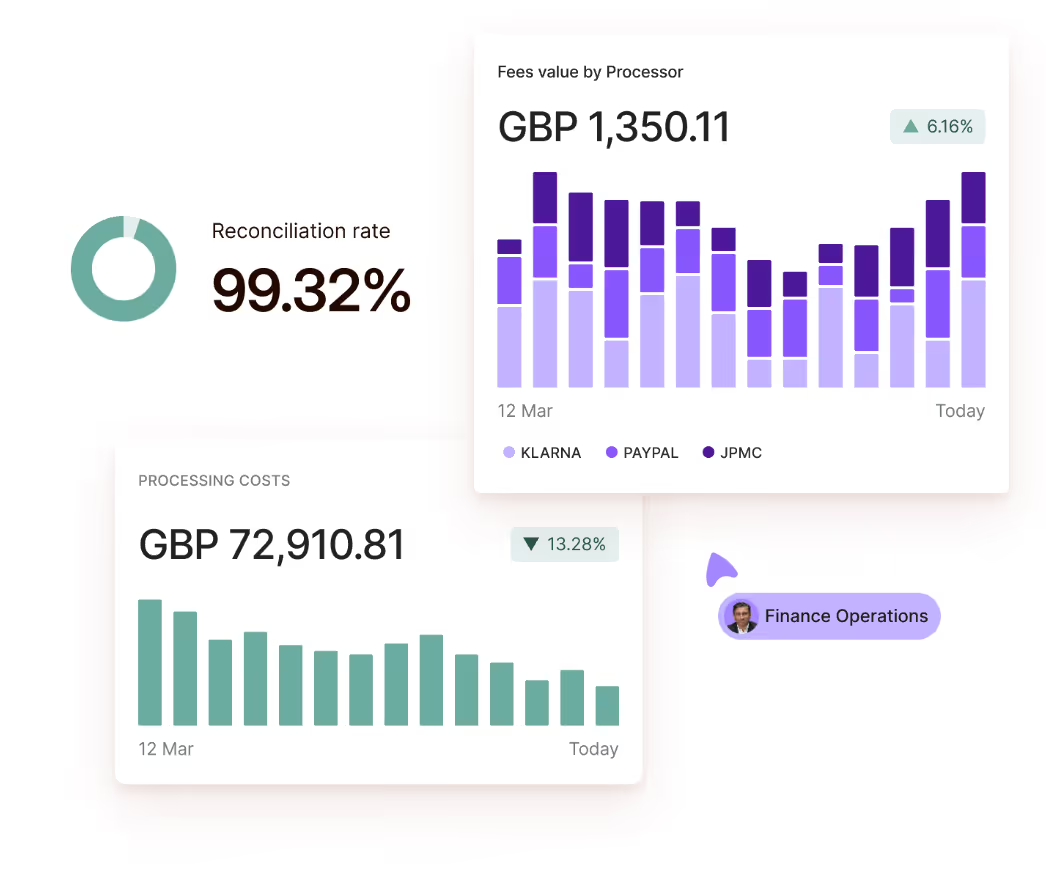

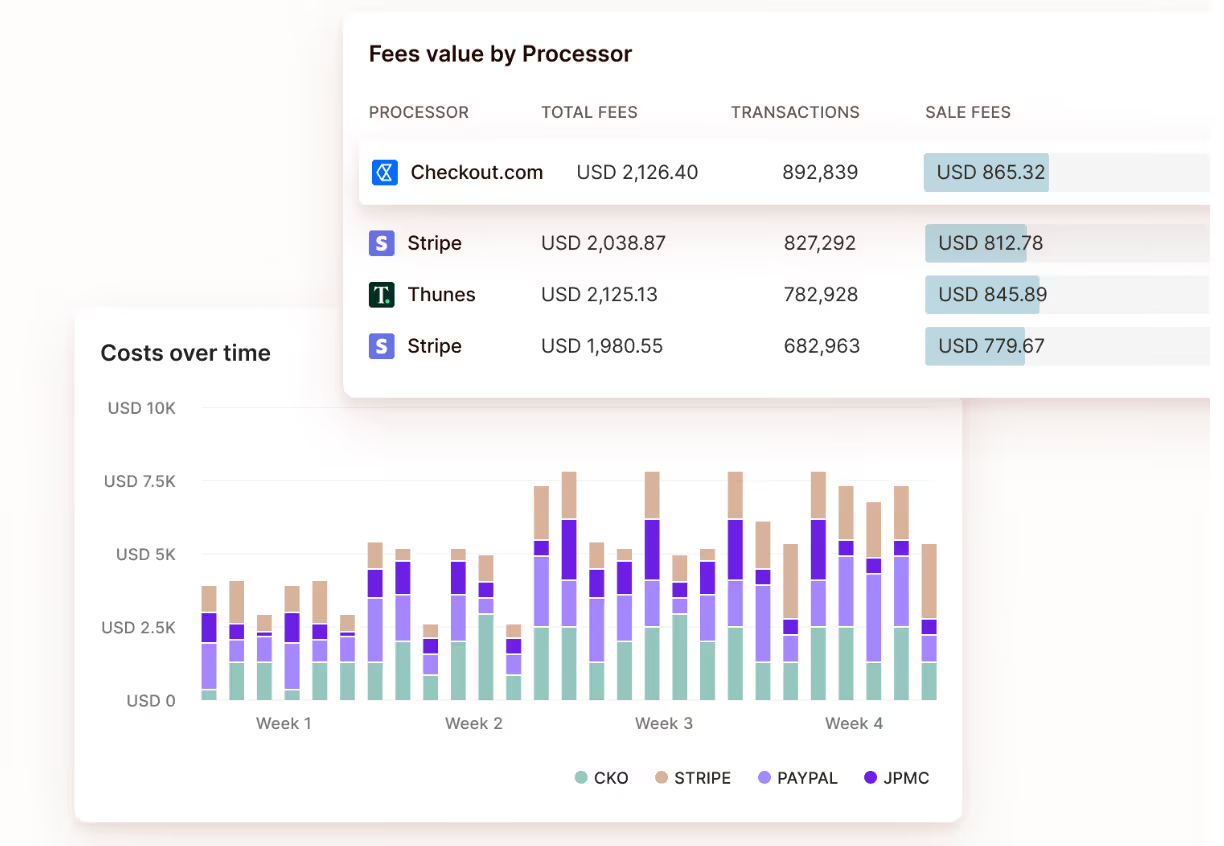

Primer’s new Costs Overview, built into Primer Reconciliation, standardizes fee reporting across all your providers into a single view. Instead of manually pulling reports from multiple PSP portals, your team can see interchange, scheme, processor, and FX fees side-by-side in one consistent format.

You can break costs down by card type, region, payment method, processor, and transaction type to understand your true unit economics in much greater detail. Costs Overview also surfaces FX markups by comparing the rate your PSP applied against the live market rate, helping you identify where cross-border transactions are quietly eating into margin.

This level of granularity makes it much easier to spot inefficiencies across your payment stack. Imagine you compare two processors handling UK debit card payments and discover Processor A is consistently charging higher processor fees than Processor B for the same transaction profile. Instead of letting that margin disappear unnoticed, you can reroute volume toward the cheaper provider directly through Primer’s orchestration layer.

And when contract renewal time comes around, you’re negotiating from a position of strength. Instead of relying on assumptions or fragmented PSP reports, you can walk into conversations with hard benchmarking data showing exactly how each provider compares across regions, payment methods, and fee categories.

Route every transaction to the ideal processor and reduce what you actually pay

Relying on a single payment provider often forces you into a one-size-fits-all fee structure that fails to account for regional or card-specific cost differences.

But with Primer Workflows, you can set up automated routing rules to minimize your card processing fees, and increase authentication rates.

For example, you might choose to route domestic debit payments in France to a local acquirer like Cartes Bancaire, leading to a lower card fee and better authentication rates than a global processor. All of this can be done in seconds, without any coding.

You can also set up Fallbacks, which automatically route any failed payments to a processor of your choice. This is how Primer customer Banxa saved US$7 million in just 6 months.

Read more: A guide to payment routing: everything you need to know

Reduce FX costs when you accept payments in multiple currencies

If you accept payments in multiple currencies, FX fees can compound as quickly as interchange. Traditional PSPs automatically convert currencies at settlement, often applying a steep markup.

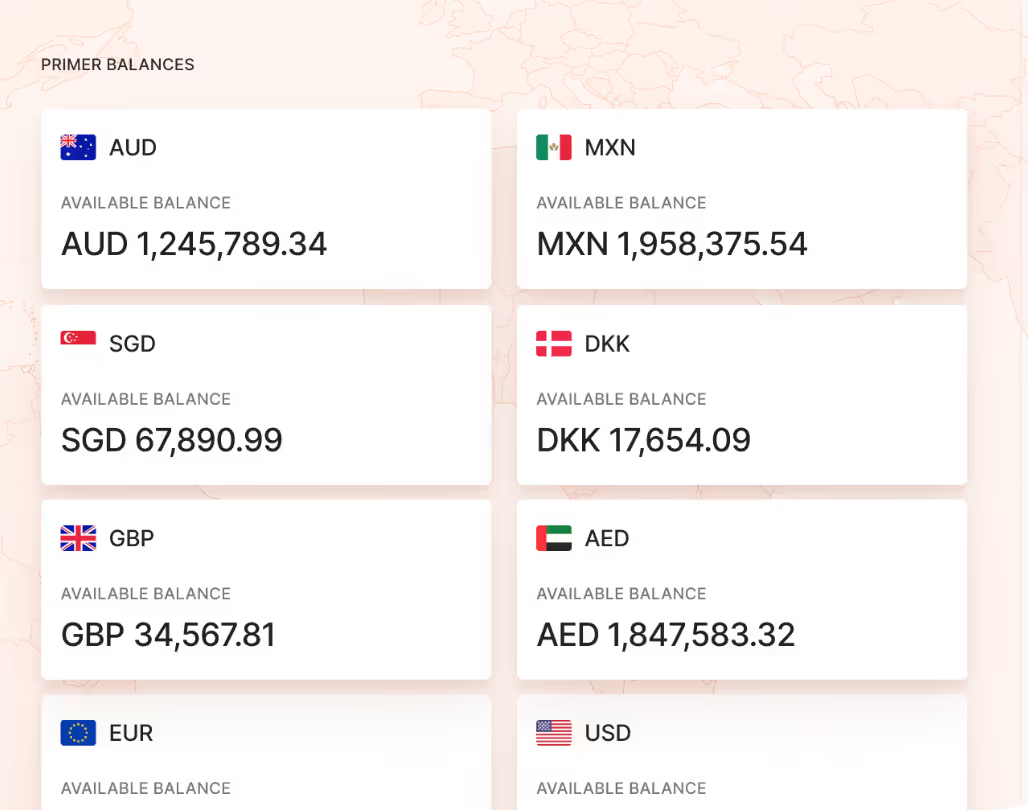

Primer’s Global Accounts allow you to hold and manage funds in 20+ currencies. You can collect in local currency, hold it, and choose when to convert it deliberately. This gives your finance team control over the conversion timeline and prevents "double dipping" on FX fees when paying international suppliers.

Primer also offers:

- Network tokenization: This enables you to lower your interchange rates on tokenized transactions and use automatic credential updates to safeguard your recurring revenue.

- Reconciliation: Access standardized cost reporting across all connected processors in a single format, eliminating the need to manually reconcile incompatible reports.

- Observability: Gain complete visibility throughout the payment stack with a 360-degree view that unifies data across every provider. Use over 100 visualizations to monitor key metrics and track cross-processor performance as it happens.

- Monitors: Set up real-time Monitors to detect issues before they compound. Receive instant alerts on cost spikes or performance drops, allowing your team to act before margins are impacted.

Take control of your payment costs with Primer

Interchange fees are the largest component of your card processing costs, but they don't have to be a black box. The pricing model you choose, the routing decisions you make, and the data visibility you maintain all determine how much of each transaction ends up as a fee rather than revenue.

Primer gives you the infrastructure to understand these costs and the tools to optimize them in real time. Book a demo to see how Primer makes payment cost management work for your business.

Frequently Asked Questions (FAQ): Interchange optimization

Are interchange fees negotiable?

No. Interchange rates are set by card networks like Visa and Mastercard and are non-negotiable. However, the processor markup and the pricing model you use are negotiable and have a significant impact on your total cost.

What is the difference between interchange fees and card processing fees?

Interchange is just one component of the total card processing fee. Card processing fees also include scheme fees (paid to the card network) and the processor’s markup (the fee for the service provided by your PSP).

Why do interchange rates vary between transactions?

Rates vary based on the perceived risk and cost of the transaction. Factors include whether the card was present, whether the card is a high-reward credit card or a standard debit card, and the merchant’s industry category.

Is interchange-plus pricing better than blended pricing?

Neither is ‘better’ than the other. IC+ is more transparent and ensures that you benefit when interchange rates drop or when you process low-cost transactions, however it adds complexity. Blended pricing is simpler but usually more expensive at scale.

How do interchange fees differ between the US and EU?

US interchange fees are generally unregulated and higher, often exceeding 2%. In the EU, interchange fees for consumer cards are capped by regulation at 0.3% for credit cards and 0.2% for debit cards.

.png)

.avif)