Every month, subscription businesses lose revenue to a preventable problem.

A card expired. A retry hit insufficient funds at the wrong time. A processor went down during a billing cycle. The customer had to authenticate twice, got frustrated, and gave up.

These payment failures are largely preventable with a good payment setup. Yet many subscription businesses end up treating all failed payments the same way.

They’ll retry blindly, hope for the best, and watch revenue leak through fixable cracks. And with avoidable failed payments causing an estimated 50% of subscription churn, your organization could be bleeding revenue.

The businesses recovering the most revenue are segmenting declines by type, timing retries strategically, keeping credentials current automatically, and removing unnecessary friction from the payment flow.

This guide will show you why subscription payments fail, what to do about each cause, and how Primer can help.

Primer is a unified payment infrastructure that can helps you stop losing revenue to preventable payment failures. Book a call with the Primer team to learn more.

Why subscription payments fail

Payment failures generally fall into two categories: soft declines and hard declines.

Hard declines are permanent. No matter how many times you retry, the payment will never go through. When you hit one, stop retrying immediately and trigger a dunning flow to collect new payment details. Common hard declines include:

- Stolen or fraudulent card

- Closed account

- Invalid card number

Soft declines are temporary and recoverable. Retry at the right time, and there's a good chance the payment goes through.

The four most common soft decline reasons are:

- Insufficient funds: The customer simply didn't have enough funds available at the time of billing. This is one of the most common soft declines and is usually recoverable within a few days once the customer's account is topped up.

- Daily spending limit reached: The customer's bank has a cap on how much can be charged in a single day. The funds are there, but the transaction is being blocked temporarily. A retry a few days later will often succeed.

- Expired or replaced cards: Banks routinely reissue cards when they expire, get lost, or are flagged for fraud. When that happens, the card details on file no longer match what the bank has, and the payment fails. Unless your system updates card details automatically, you're dependent on the customer doing it themselves, which many never get around to.

- Authentication friction: Some payment failures trigger a re-authentication step, where the customer is asked to verify their identity before the payment can go through. If that request comes at the wrong moment, or the customer doesn't notice it, the payment stalls. What started as a fixable failure becomes a lost subscriber.

Four common mistakes subscription merchants make (and what to do instead)

1. Treating soft and hard declines the same

Treating every failure the same wastes resources and loses revenue you could have recovered. Retrying a hard decline won't work, and doing it repeatedly can result in fines. Failing to retry a soft decline means losing revenue that was recoverable.

The fix is to build retry logic around specific decline codes rather than applying a one-size-fits-all rule. For example, an insufficient funds decline might warrant a retry in three to five days. A stolen card should trigger a dunning flow asking for new payment details, with no retries at all.

2. Letting expired cards rely on customer action

When a customer gets a new card, updating their billing details across every subscription they have is rarely a priority. Most intend to get around to it, and many never do. A payment failure that should have been invisible becomes a cancellation.

Network tokenization solves this without involving the customer at all. Instead of storing a card number, you store a token issued by Visa or Mastercard. When the underlying card is renewed or replaced, the network updates the token automatically. The next billing cycle goes through as normal, and the customer never needs to do anything.

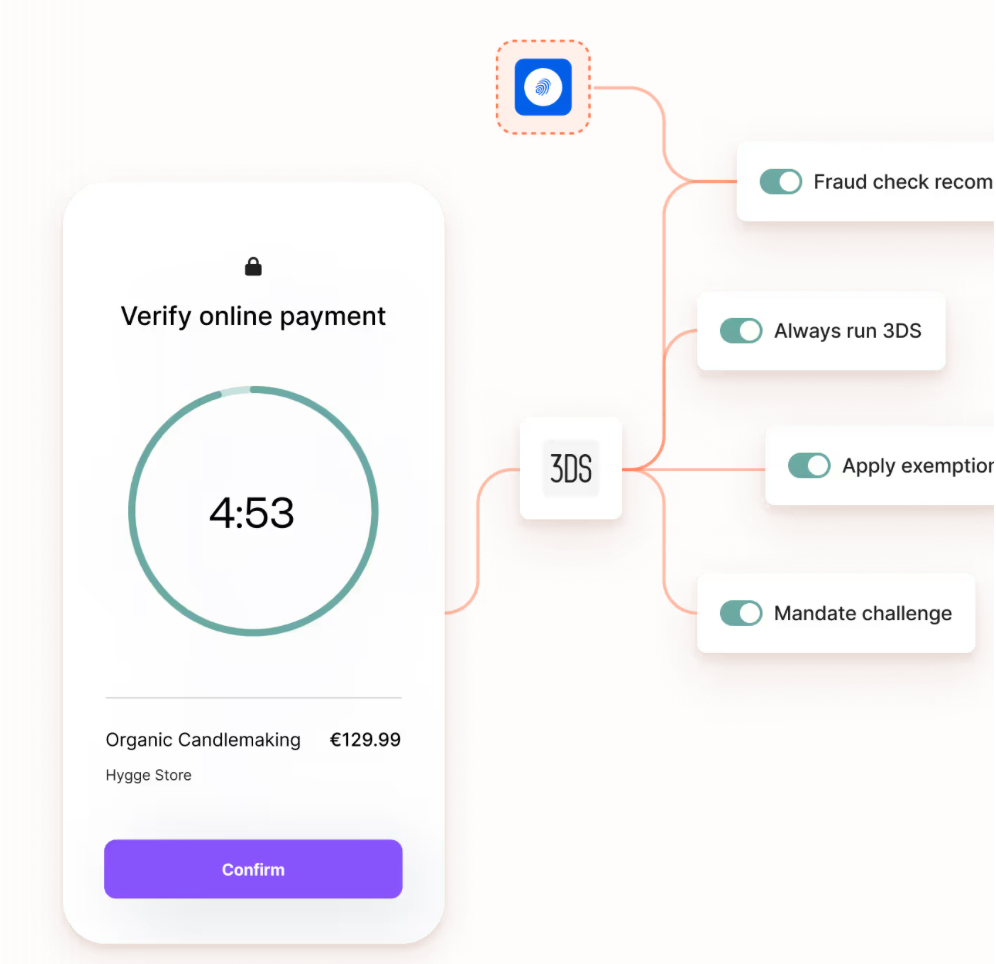

3. Forcing customers to re-authenticate on every retry

3D Secure is the authentication step customers know as the code sent to their phone, or the fingerprint prompt, before a payment goes through. It exists for good reason, but it creates a problem when a failed payment needs to be retried.

If your system asks the customer to authenticate again every time a retry is attempted, most won't bother completing it. A payment failure that was entirely fixable on your end becomes churn because of unnecessary friction.

A smarter approach carries the original authentication result across processors, so the customer isn't asked to verify again just because the payment is routed through a different processor the second time. For recurring subscriptions, many issuers already allow subsequent charges to go through without re-authentication once the initial transaction has been verified.

4. Relying on a single payment processor

When your primary processor goes down during a billing cycle, every renewal attempt fails at once. Outages can last minutes or hours, and they don't come with advance notice. For a subscription business running large billing cycles, that's a wave of simultaneous failures that your team has to chase manually, and some customers won't come back once their access lapses.

The solution is processor redundancy with automatic fallbacks. If the primary processor fails, the payment routes to a secondary processor in real time, with no action required from the customer. For soft declines where both processors are unavailable, retry logic kicks in based on the specific decline code. For hard declines, retries stop immediately, and a dunning flow is triggered to collect new payment details.

How Primer’s unified payment infrastructure can help you manage payment failures

Primer is a unified infrastructure platform that connects your business to a range of local and global payment processors, payment methods, and fraud tools that you can manage in one place.

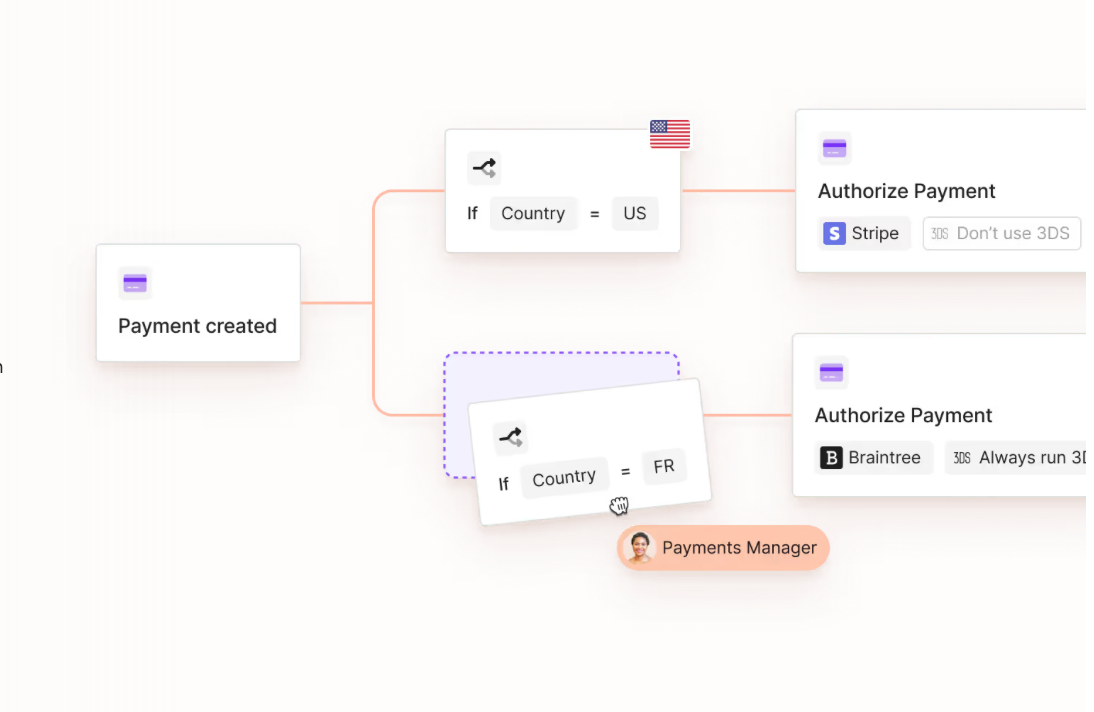

Instead of building and maintaining separate integrations for each processor, your payments team controls everything through a single platform, including retry logic, fallback routing, and 3DS rules, without writing a single line of code.

Configure intelligent retry logic without any coding

Primer Workflows lets you build automated retry rules based on specific decline codes using a drag-and-drop interface that doesn’t require a single line of code.

Here’s an example workflow:

- Payment fails with "insufficient funds" → Wait five days, retry once

- Payment fails with "do not honor" → Wait seven days, retry once

- Payment fails with "stolen card" → Never retry, trigger dunning email

- Retry fails → Route to backup processor automatically

- All retries exhausted → Trigger final dunning sequence

Your payments team can configure this logic independently without pulling engineers away from product development. When you need to adjust retry timing or add a new processor to the fallback chain, you update the workflow in minutes.

Keep payment credentials current without asking customers to lift a finger

Network tokenization is built into Primer. When you store a customer's payment details, Primer replaces the card number with a secure network token issued by the card networks (such as Visa or Mastercard). This token acts as a surrogate for the underlying card but remains linked to it within the network.

Because the token is managed directly by the card networks, it can automatically update when the underlying card changes — for example, when a card expires, is reissued after loss or fraud, or is upgraded by the issuer.

That means subscriptions and stored payment methods continue working without interruption. Updates happen behind the scenes without any action from the customer, eliminating card expiry and reissuance as common sources of involuntary churn.

With Primer handling tokenization, you also avoid the complexity of building your own token lifecycle management or maintaining separate integrations with each card network.

Switch processors automatically when one goes down with Fallbacks

If your primary processor fails (due to downtime, rate limiting, or any other reason), Primer can automatically route the payment to a backup processor of your choice in real time using Fallbacks. And because Primer 3DS is agnostic, your customers won’t have to complete another 3DS check, meaning the entire process is completely invisible to them.

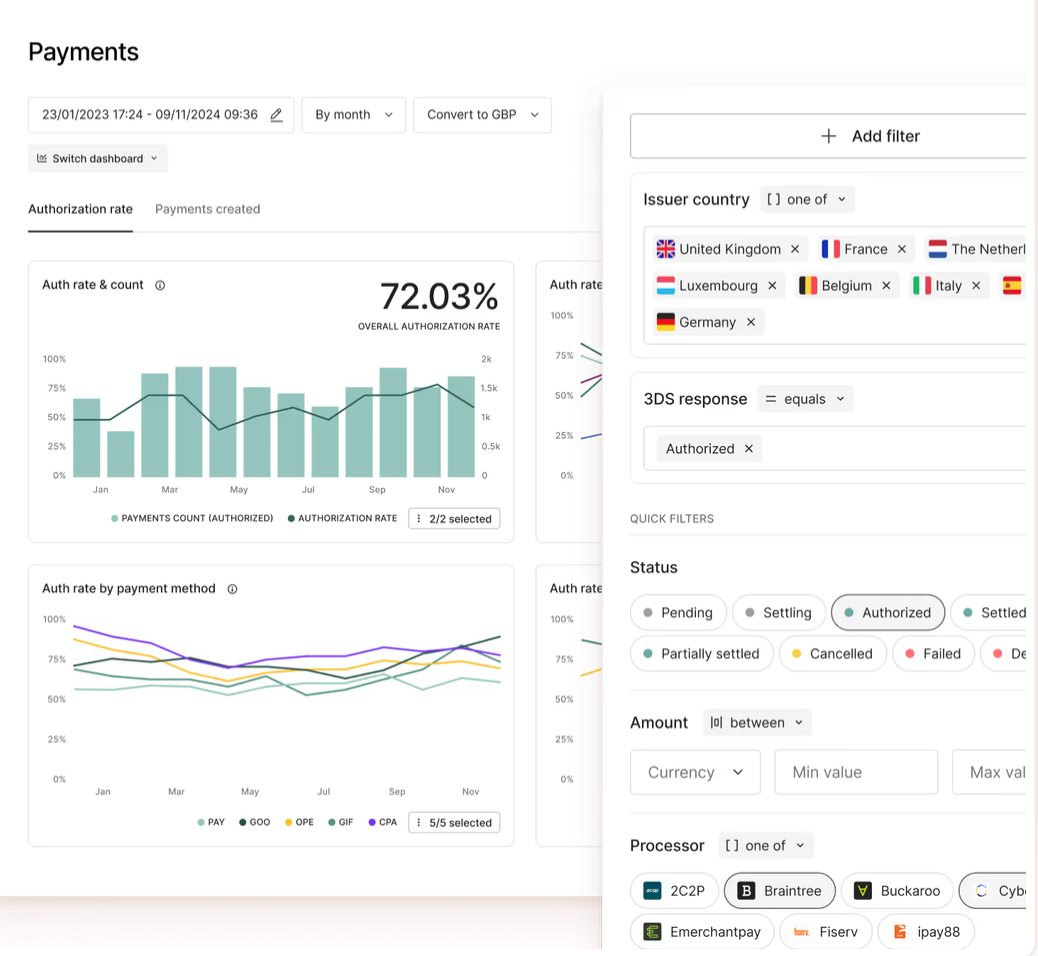

Pinpoint exactly where and why payments are failing

Primer Observability gives you a single view across all processors. You can see:

- Which decline reasons are driving failures: Primer unifies decline codes across processors and payment methods, helping you analyze decline patterns and identify issues that may need different recovery actions.

- Authorization rates by processor and payment method: This helps you spot underperforming providers or payment methods, and optimize routing decisions accordingly.

- How payment optimization changes are performing: Use Observability to analyze the performance of different payment setups and A/B tests, so you can compare outcomes and refine your strategy over time.

- Where recovered revenue is coming from: The Sales Recovery dashboard shows the value, count, and rate of payments recovered through Primer, including recovery via Fallbacks.

Without this visibility, you're operating blind. With it, you can identify patterns and optimize your recovery strategy based on real data.

Stop losing revenue to preventable payment failures with Primer

Primer enables you to implement sophisticated recovery strategies without requiring specialized payment engineers. Your payments team gets full control over retry logic, fallback routing, and authentication flows, and it all happens through visual workflows that don’t require any coding.

Book a demo to discover how Primer's unified payment infrastructure can help you recover more revenue, reduce involuntary churn, and scale efficiently.

Frequently asked questions

What is the difference between a soft decline and a hard decline in subscription payments?

A soft decline is a temporary payment failure that may succeed if retried, often caused by insufficient funds or temporary payment processing issues.

A hard decline is a permanent rejection, such as a closed account or invalid credit card, meaning retrying the transaction will not succeed.

What are the most common reasons for failed subscription payments?

Some of the most common reasons include expired credit cards, insufficient funds, fraud checks, card declines, or technical issues with payment gateways and processors.

How do network tokens help reduce subscription payment failures?

Network tokens replace stored credit card numbers with secure tokens issued by card networks. When a card expires or is replaced, the network updates the token automatically, helping prevent failures caused by expired credit cards in recurring billing. Platforms like Primer support network tokenization to help reduce these types of payment failures.

What is involuntary churn?

Involuntary churn occurs when a customer wants to continue using a subscription service, but payment issues or failed subscription payments cause the subscription to lapse. If these failed transactions are not recovered, they can lead to significant lost revenue.

How can businesses recover failed subscription payments?

Businesses can automate their payment recovery process using payment retries, customer notifications, and follow-ups via email or SMS. Using platforms like Primer can also help automate retries and route payments through different payment gateways to improve recovery rates.

Why are payment retries important for recurring payments?

Most failed subscription payments aren't permanent. They can be caused by temporary issues like insufficient funds or expired cards. Retrying at the right time recovers a significant share of that revenue automatically, without any friction for the customer or manual work for your team.

How do failed subscription payments affect customer lifetime value?

When failed transactions are not recovered, customers may churn unintentionally. This lowers customer lifetime value, weakens customer relationships, and impacts long-term customer retention.

What metrics should subscription businesses track for payment failures?

Important metrics include failure rates, authorization rates, recovery rates, and the percentage of failed subscription payments successfully recovered. Tools like Primer Observability help teams monitor these metrics across processors and payment methods.

Can offering alternative payment methods reduce payment failures?

Yes. Supporting alternative payment methods alongside credit cards can reduce dependency on card payments and improve success rates for recurring payments, especially in ecommerce subscriptions.

.avif)

.avif)