Stripe is one of the most popular payment service providers (PSPs), and for good reason. Its developer experience is excellent, its documentation is thorough, and getting up and running is straightforward. For businesses in the early stages of growth, it's often the right starting point.

However, as your business scales or expands into new markets, you may find yourself looking to complement Stripe with additional processors. A single PSP, however reliable, limits your ability to add redundancy, optimize fees across different regions, or access local payment methods that can lift conversion in specific markets.

And the concern around single-processor dependency is widespread: in our survey of 150 payments leaders, 93% said relying on one processor worries them. These are outcomes that only a multi-PSP strategy can deliver.

Primer is a unified payment infrastructure that can help you stop losing revenue to preventable payment failures. Book a call with Primer to learn more.

Stripe alternatives in the US

Braintree (PayPal)

Braintree, owned by PayPal, is a strong option for businesses with significant digital wallet volume. Its native support for Venmo and PayPal makes it particularly useful for US e-commerce, where both methods have strong adoption rates.

Braintree's standard rate of 2.89% + $0.29 per transaction is slightly cheaper than Stripe's 2.9% + $0.30. At higher volumes, Braintree offers custom flat rates and interchange-plus pricing for established businesses, which can become more cost-effective.

Checkout.com

Checkout.com may be well-suited for businesses that want more control over how their payments are routed and managed.

Rather than a fixed published rate, this PSP offers either fully flat-rate pricing based on business profile and risk category, or interchange-plus pricing that passes through card association, processor, and interchange fees transparently.

Both models could make it more cost-effective than Stripe at scale, particularly for businesses that want granular visibility into what they're actually paying per transaction, thanks to the platform’s detailed analytics. Checkout.com also has good global reach, making it a reliable choice for those who want to expand into new markets.

Stripe alternatives in Europe

European payment processing has its own set of requirements. Local payment methods vary by country, and processors with strong local issuer relationships can achieve better authorization rates in their home markets. Here are the leading options for Stripe alternatives in the EU.

Adyen

Adyen is based in Amsterdam and is a leading option for European payment processing. Its relationships with European card networks and issuers translate into authorization rates that can outperform global processors in markets like Germany, France, and the Netherlands.

Adyen supports all major local payment methods across the region, and its interchange-plus pricing model — a fixed processing fee plus the actual interchange cost — becomes increasingly cost-effective at scale.

Mollie

Mollie is a strong Stripe alternative for businesses targeting the Benelux region and broader European markets. It offers deep local payment method coverage, particularly for the Netherlands, Belgium, and Germany. Mollie offers both a standard pricing option and a volume pricing option based on an interchange ++ model.

While Mollie operates at a smaller scale than Adyen, it can be well-suited to businesses with a focused European presence rather than those with global processing needs.

Stripe alternatives in APAC

APAC presents arguably the most complex payment landscape of any region. Payment methods vary dramatically by market. Alipay and WeChat Pay are popular in China, for example, and Konbini and carrier billing are big in Japan. No single processor offers the deepest local integration across all of these markets, which means multi-PSP strategies are essential.

Adyen

Adyen has a strong APAC presence and supports major regional payment methods, including Alipay, WeChat Pay, and GrabPay. For businesses needing broad APAC coverage from a single processor, it's the most consistent global option, though local specialists often have deeper integrations in specific markets.

2C2P

2C2P is a Southeast Asia specialist with deep integration into local payment methods, with over 400 payment method options. It can outperform global processors on both coverage and authorization rates in the area, and has over 600,000 APM acceptance points and over 400,000 payment channels in Asia.

Razorpay

Razorpay is a leading payment gateway in India, with comprehensive support for UPI and local payment methods that many global processors would struggle to match in depth. For businesses specifically targeting the Indian market, it's the clear specialist option.

Why one payment processor isn't enough

No single processor is built for every market, transaction type, or business model. The same one that delivers excellent authorization rates in Germany may not perform as well in Southeast Asia, and one best suited for digital wallet volume may not offer the enterprise analytics a scaling business needs.

There's a commercial argument for leveraging more than one payment processor, too. When you process entirely through one provider, you have no negotiating leverage. The PSP knows that switching would typically require months of engineering work, so there's little incentive to offer better rates.

The traditional answer to this problem is to pick the best single option and accept the trade-offs. However, the better solution is to use multiple processors strategically, routing each transaction to the provider most likely to succeed in that context.

A multi-PSP setup changes that dynamic, offering the following benefits:

- Cost optimization through negotiating leverage. When you're locked into Stripe alone, it’s difficult to negotiate better rates. With multiple PSPs, you can A/B test processors, shift volume based on performance, and negotiate more successfully.

- Geographic optimization. Different processors excel in different regions. You may want to use Stripe for US payments, Adyen for Europe, and regional specialists for APAC. This could help increase authorization rates and revenue.

- Redundancy and fallbacks. Single-PSP dependency creates a single point of failure risk. With a multi-PSP and fallback setup, transactions can automatically retry through Adyen or Braintree if Stripe declines or goes down.

- Feature access. Different processors offer different capabilities. Some may have better fraud tools, superior subscription management, or payment methods global players don't support. By working with multiple PSPs, you can take advantage of the key features of each.

No single processor is best everywhere, so relying on just one is always a compromise.

The barrier has historically been engineering complexity. Each processor comes with its own API, webhook format, and data model. Building and maintaining separate integrations for two or three processors multiplies that burden significantly. It's why most businesses default to one provider and accept the trade-offs rather than tackle the overhead of managing several.

That's the problem Primer solves.

How to easily manage multiple PSPs with Primer

You only need to integrate once with Primer, and then you can activate any connected processor through the dashboard. No additional engineering required. This means adding a new PSP is possible within hours, instead of taking months. Primer also handles API differences, data standardization, and ongoing maintenance, so you won't need ongoing internal support.

Here’s how it works.

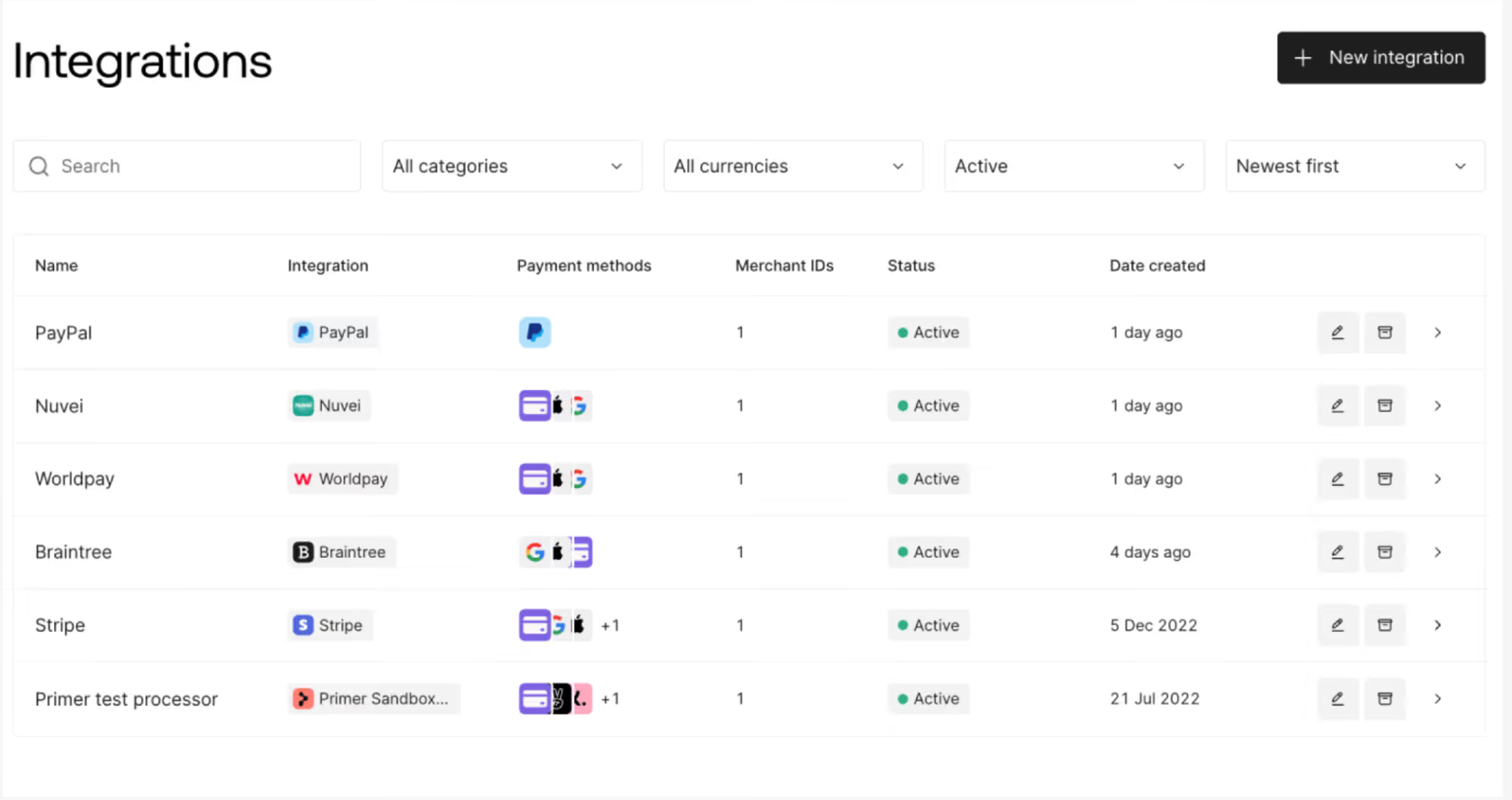

Step 1: Connect your PSPs to Primer

In the Primer Dashboard, navigate to the Integrations section and select the processors you want to activate. You’ll then give Primer access to the PSP account and log in to your merchant account.

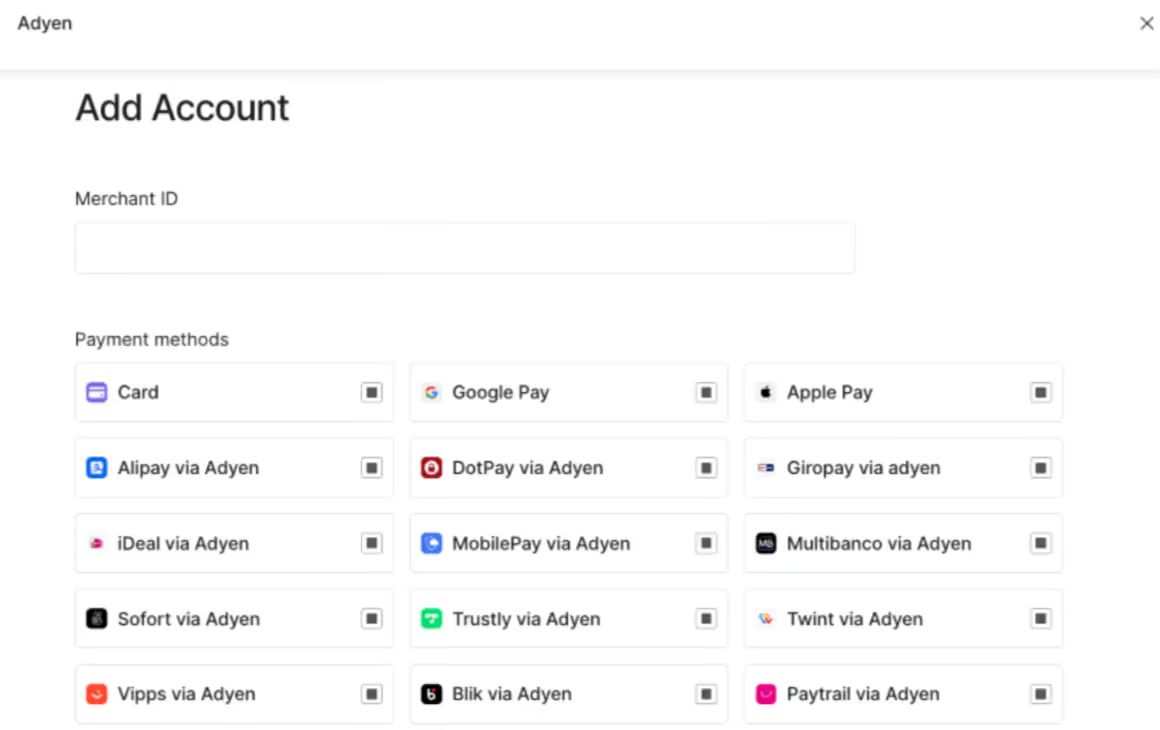

Step 2: Enable payment methods for each PSP

You can customize payment methods for each PSP. On Adyen, for example, you can choose to accept cards and Google Pay, but you may choose to only allow cards, PayPal, and Venmo on Braintree. If certain processors offer more competitive rates on different payment methods, you can use this to your advantage.

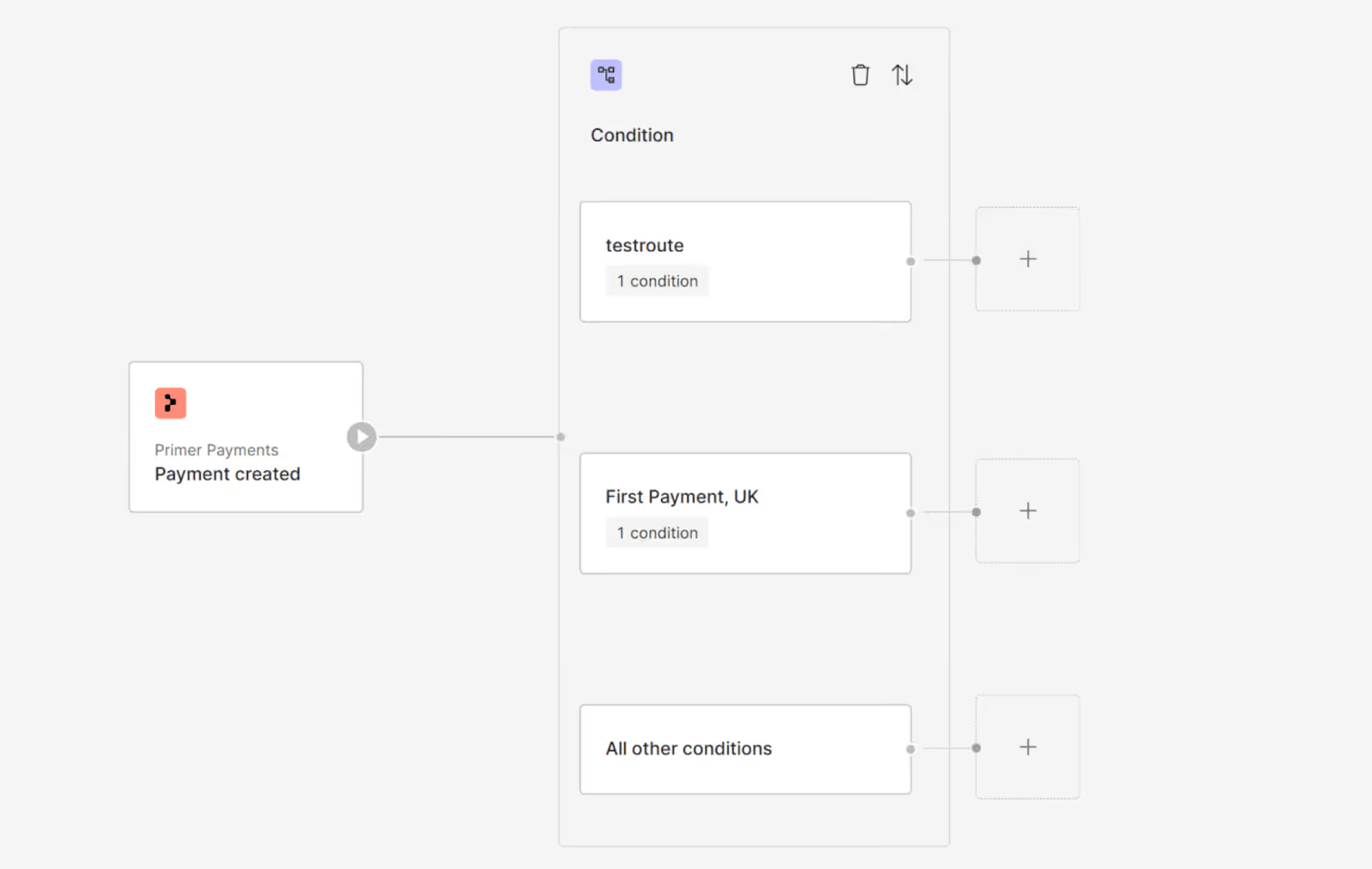

Step 3: Configure routing logic in Workflows for payment optimization

Navigate to Workflows in the Dashboard and build your routing logic visually using the drag-and-drop builder. Rules can be set by geography, transaction value, payment method, or any combination of factors.

For example, you might route most European transactions through a regional processor while keeping US volume on Stripe, or send higher-value transactions to a processor with better rates at that tier. No engineering ticket required.

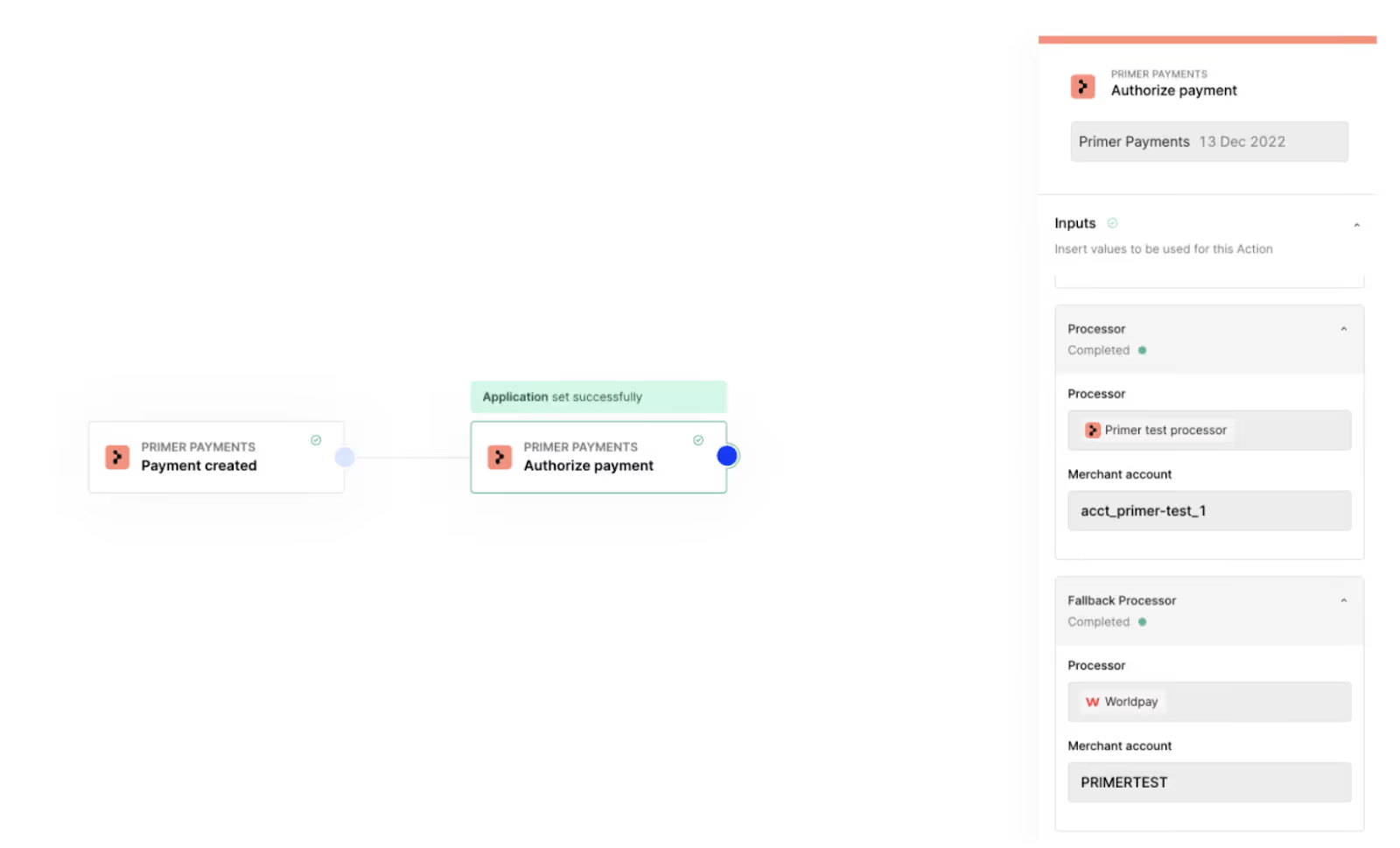

Step 4: Set up Fallbacks to prevent lost sales

Within the same Workflow, configure fallback logic. This way, if your primary processor declines a transaction or experiences downtime, Fallbacks automatically retries through an alternative processor.

Step 5: Monitor performance across all PSPs with Observability

Once live, Primer Observability provides a unified view across every connected processor. You can see authorization rates, processing costs, and performance by region and payment method in a single dashboard. From here, you can identify where to adjust routing, spot performance issues before they compound, and build a data-driven case for PSP rate negotiations.

Maximize your PSP strategy with Primer

Setting up multiple processors is only the starting point. Primer's platform gives payment teams the tools to optimize routing, protect revenue, and make data-driven decisions, without relying on engineering for every change.

You can also use:

- Workflows to route transactions to the right processor, without writing code

- Observability to analyze the results across every connected processor in real time. Monitors can be configured to send automated alerts when authorization rates drop below a defined threshold, so performance issues are caught before they compound.

- Network tokenization to replace stored card numbers with tokens issued by Visa or Mastercard, which automatically update when a card expires or is reissued. This reduces involuntary churn on recurring payments and improves authorization rates, since processors typically prefer tokens over raw card data.

- Global Accounts to hold and manage funds in 20+ currencies from a single dashboard, reducing forced currency conversions and the FX fees that come with them. For enterprises with significant cross-border volume, this is a meaningful reduction in cost that grows with scale.

- Reconciliation to pull transaction data from every connected processor into a standardized format, accessible from one dashboard. This means your finance team can work from a single report rather than logging into multiple PSP dashboards and reconciling incompatible data formats.

- AI Companion, Primer's newest product, for AI-powered guidance that helps your team make faster, more informed decisions, without making changes automatically.

How Banxa recovered US $7M in revenue with Primer’s Fallbacks

Banxa is a leading crypto infrastructure provider, operating the on- and off-ramps that allow users to convert fiat currency into crypto across major platforms. As it scaled, Banxa's payment stack had grown with multiple processors and payment methods without a clear strategy. This resulted in a system that was difficult to manage and optimize.

The team had suspected some payments were being incorrectly declined, but they had no visibility into the scale of the problem.

After implementing Primer, Banxa recovered over $7 million in revenue in the first six months using Primer's native Fallbacks functionality. After enabling Fallbacks, Primer's decline code mapping then targeted transactions likely to succeed with an alternative processor, recovering revenue that had previously been written off.

"The transition to going live was seamless, and the results have been immediate and overwhelmingly positive. Our conversion rates have increased, and our customers are noticing the difference. And they're sending more volume our way." — Greg Rikkhachai, Head of Payments, Banxa

Build a multi-PSP strategy with Primer

A multi-PSP strategy allows you to get better regional coverage and stronger payment method support while you get a fallback layer that protects revenue if a single processor experiences downtime.

Primer makes that strategy manageable without ongoing engineering overhead. One integration gives access to a range of local and global payment processors.

Book a demo to discover how Primer's unified payment infrastructure can help you expand payment options, reduce costs, and scale faster.

Frequently asked questions (FAQ): Stripe Alternatives

Should I replace Stripe or add alternatives alongside it?

For most businesses, adding alternatives alongside Stripe is the better approach. Stripe handles certain online payments, including credit card and debit card transactions, very well in some markets. However, gaps such as regional authorization rates, local payment method coverage, and single point of failure risk are better addressed by adding more processors rather than replacing Stripe entirely.

How do I manage multiple payment processors without massive engineering work?

The traditional approach to managing multiple payment systems requires building and maintaining separate integrations for each processor, which significantly increases engineering complexity.

Unified payments platforms solve this with a single integration that unlocks connections to multiple providers. With Primer, for example, you can activate new processors quickly and accept payments across different regions without additional engineering resources.

Which Stripe alternative is best for my business?

The best Stripe alternative depends on where you process online transactions and what you're optimizing for. Regional processors often outperform global providers on credit card authorization rates, local payment method coverage, and transaction fees in their home markets.

The most effective approach is to identify where Stripe's gaps are most costly and add a processor that addresses those specific issues.

How can I save more by working with multiple payment processors?

When you use multiple payment processors, you can reduce the overall cost of your card and online payments for several reasons:

- Higher authorization rates can increase the number of successful online transactions

- Lower transaction fees can be negotiated when routing volume strategically

- Fallbacks help recover revenue from failed credit card payments

At scale, this leads to meaningfully lower costs and improved revenue performance.

Can I add other processors if I’m already integrated with Stripe?

Yes, you can add other processors even if you’re already using Stripe. With Primer, your existing Stripe setup continues to handle the online payments it’s configured for, while additional providers can be layered in to optimize performance, coverage, and payment solutions across different markets. There’s no need to rebuild or replace your existing integration.

.png)

.avif)