Not long ago, most merchants could get by with a single PSP. One provider, one connection, one dashboard. But global commerce has changed. Customers expect to pay with local methods wherever they are, card schemes and regulations vary by region, and new providers are constantly emerging.

Managing payments now means juggling multiple providers, payment methods, and markets: each with its own rules, integrations, and reporting. Many merchants try to solve this with payment orchestration, which helps route transactions intelligently. But orchestration alone rarely goes far enough. You can still end up managing separate dashboards, fragmented data, and disconnected tools that make optimization slow and costly.

This is where unified payments infrastructure comes in. Instead of stitching together point solutions, it gives you one connected platform to manage the entire payment lifecycle, from processing and routing to fraud, reconciliation, and analytics.

Looking to see how a platform like Primer can help turn payments into a true growth driver? Book a demo today

Payment orchestration vs payment infrastructure providers

Payments are complex. If you want to rely on more than one PSP (and you should), you're going to be facing significant engineering resources to manage a fragmented payment stack.

This is where payment orchestration shines. Payment orchestration gives you the power to set up smart payment routing: directing transactions to the most suitable payment processor based on factors like geography, card type, transaction value, or performance metrics.

However, you may still wind up having to work with other tools or build additional code. For instance, if you want to configure specialized fraud engines, normalize data across providers, or analyze performance comprehensively, you can still end up with multiple logins, dashboards, tools, and sources of truth.

A payment infrastructure platform aims to offer what orchestration does, plus additional tooling to help you solve as many of your payment problems in one place as possible.

What is a payment infrastructure platform?

There is no one-size-fits-all definition of a payment infrastructure platform. In our view, it should put everything that touches payments under one roof.

This includes payment routing, fraud prevention, authentication, reconciliation, analytics, and optimization tools: all working together seamlessly rather than as siloed point solutions.

In theory, you can create this yourself. But it's a significant undertaking that requires substantial engineering resources, ongoing maintenance, and deep payments expertise. A unified infrastructure platform offers you this functionality without needing to build it in-house.

A payment infrastructure platform is more like a blank canvas than a prescriptive service: a place to create your own vision for exactly what your payments should look like, without needing extensive coding (or any coding) or developer resources.

It gives you all the tools to build a flexible payment stack that scales with your business, all in one central, interconnected, intuitive platform.

When is the right time for merchants to use a payment infrastructure solution?

The best time to start using a payment infrastructure platform is during early growth stages, before you start accruing technical debt from multiple point solutions and fragmented integrations.

Many businesses wait until they're experiencing pain from their existing setup; juggling multiple provider relationships, struggling with data silos, or hitting engineering bottlenecks for basic payment optimizations. By then, migration becomes more complex and costly.

Starting with a unified approach from the beginning allows you to scale more efficiently, experiment faster, and avoid the operational complexity that comes with managing multiple payment tools.

What to look for when assessing a payment infrastructure platform

- Reliability: Your platform should be enterprise-ready, tested, and proven with high-performing, ambitious businesses. Look for providers with strong uptime guarantees and a track record of handling high transaction volumes.

- Flexibility: Your platform shouldn't be prescriptive: for example, only letting you use certain payment methods or built-in workflow options. It should give you the freedom to build the way you need to build, adapting to your specific business requirements rather than forcing you to adapt to platform limitations.

- Intuitive and accessible: The platform should be easy enough that anyone on your team with a good idea can use it, while also serving users with deep technical expertise. Non-technical team members should be able to make configuration changes, run experiments, and optimize flows without always needing developer support.

- Developer-friendly when needed: Unlike some payment orchestration tools that operate as black boxes, a payment infrastructure platform should let your developers "open the box" and experiment with unlimited flexibility when technical customization is required.

- Comprehensive tooling: Look for a wide range of tools, systems, and optimization capabilities so you can optimize every aspect of your payment stack, from routing and fallbacks to fraud prevention and reconciliation.

- Unified data and analytics: A single source of truth for all payment data, with the ability to test and optimize based on comprehensive insights across all your providers and payment methods.

- Seamless connectivity: Your infrastructure can't exist in isolation. It needs to integrate smoothly with your existing systems, from your e-commerce platform to your CRM, accounting software, and business intelligence tools.

- Expert support and guidance: You want payments experts on your side to help you grow. Look for providers who will help you spot opportunities, build new solutions, and optimize performance, acting as an extension of your team rather than just a vendor.

- Built for scale: Your infrastructure should help you scale, not limit you. As you become more complex, you shouldn't be held back. You should be able to add more payment methods, build sophisticated flows, and connect to different systems seamlessly.

Why use Primer as my payment infrastructure?

Primer has built the world's first unified payment infrastructure platform, designed specifically to give merchants complete control over their entire payment stack. Here’s how we help merchants revolutionize their approach to payments:

Putting payment leaders in control

Most payment solutions require deep domain expertise to use effectively. Primer changes this by giving payment managers full control after a one-time engineering integration. They can add new services, create workflows, run experiments, and optimise performance without relying on developer time.

As Lucas Quinio, Head of Payments at Conforama, puts it: “Primer breaks the mold. Most solutions require specialist knowledge just to operate. Primer actually empowers the team.”

Read more: Reimagining the role of payments at Conforama

Standardizing the language of payments

Learning payments is like learning a new language, and each PSP speaks a different dialect. Stripe calls it a "payment intent," Adyen calls it a "transaction," and Checkout.com calls it a "payment." This complexity multiplies across every aspect of payments.

Primer solves this by creating a unified abstraction layer. We've built standardized integrations with 100+ payment services, translated all the different data formats, and created one consistent language for managing payments. You only need to learn how Primer works, not how every individual provider operates.

Enabling teams across the business

We don't just serve payments teams. We enable finance, operations, product, customer support, and engineering teams to use payments strategically. For example, finance teams use Primer to streamline reconciliation, reducing time spent from days to minutes. Customer support teams build VIP experiences that boost satisfaction. All without needing specialized payments knowledge.

Don’t just take our word for it:

- Ferryhopper, which operates in 12 countries with more than 100 ferry providers, uses Primer to expand globally while keeping costs and performance in check.

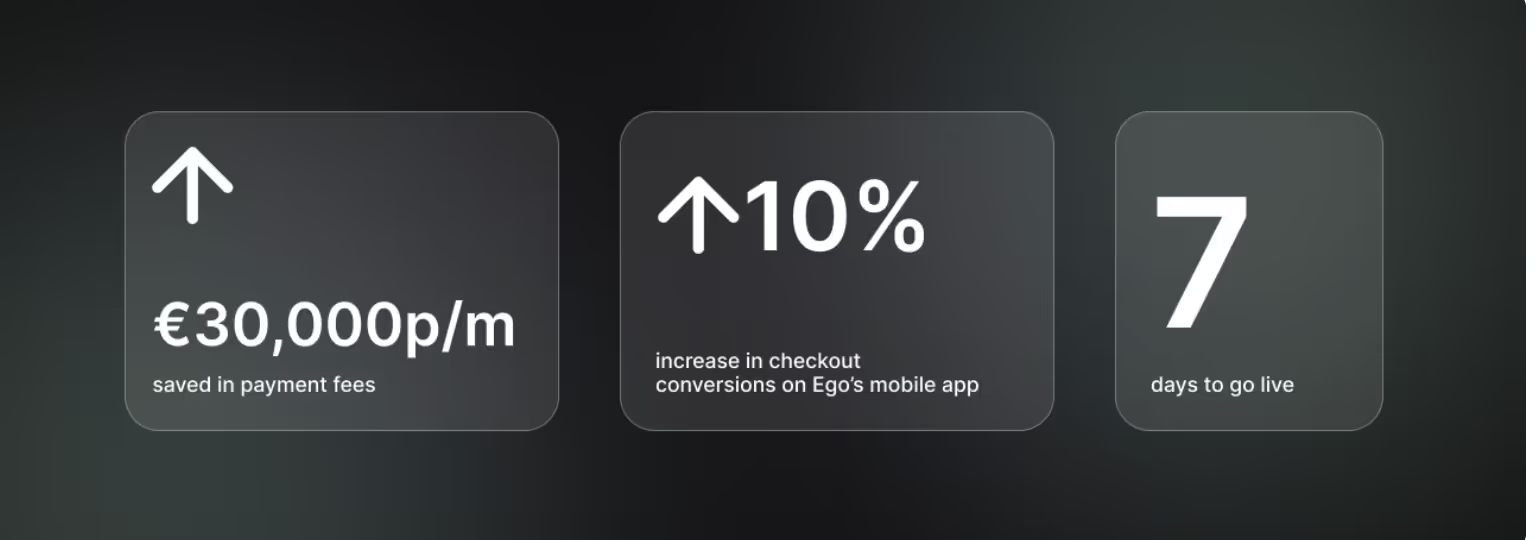

- Ego, a leading fashion brand in Europe and the U.S., went live with Primer in just a week when high PSP fees threatened its margins. The switch now saves Ego around €30,000 a month, while also lifting conversion rates by 10% on its app, even before fully customizing checkout.

- In Australia, Dabble used Primer to achieve a 96% authorization rate and recover nearly US $50,000 in failed transactions through Fallbacks during a peak period. With Primer, the team also cut its U.S. market expansion timeline from months to just six weeks.

Use Primer to take control of your payment strategy

At Primer, we’re transforming how businesses think about and use payments. We envision a world where payments become the strategic heartbeat of a business, used by teams across the organization to optimize, innovate, and accelerate growth.

Ready to see how unified payment infrastructure can transform your business? Get in touch with our payment experts.

FAQ: Choosing a payment infrastructure provider

1. How is a payment infrastructure platform different from a payment gateway?

A payment gateway lets merchants accept card payments or digital wallets through one provider. A payments platform, like unified payment infrastructure, connects multiple gateways, acquirers, and payment service providers (PSPs) in one place. This gives merchants more flexibility, better authorization rates, and access to global payment methods without needing to build every API integration in-house.

2. Can unified payment infrastructure handle both online payments and in-person transactions?

Yes. Modern payment systems are built to unify online payment flows, mobile checkouts, and in-person point-of-sale (POS) transactions. So you can connect credit card, debit card, direct debit, and even real-time bank transfers into a single merchant account setup. Managing both channels under one platform simplifies reporting and ensures a consistent customer experience.

3. How does unified infrastructure help reduce transaction fees?

When you only work with one provider, you’re locked into their pricing structure. With a payments platform that unifies multiple gateways, you can route card, banking, and cross-border payments through the most cost-effective option in real time. This flexibility reduces transaction fees, improves cash flow, and helps merchants scale without adding unnecessary overhead.

4. Can I connect open banking and other alternative payment options?

Absolutely. A good payment infrastructure platform makes it simple to add open banking, PayPal, SEPA bank transfers, and other local payment options alongside traditional card networks. Instead of separate plugins or fragmented integrations, these are all managed in one place, giving customers more choice while keeping your payment flow streamlined.

5. Is unified payment infrastructure secure and compliant?

Yes. Providers like Primer build compliance into the core of their payments platform. That includes meeting PCI DSS requirements, protecting customer data, and supporting fraud tools and chargeback management. Merchants can automate workflows across payment networks while staying fully compliant with financial services regulations in the United Kingdom, Europe, and beyond. Primer is also SOC 2 Type II compliant.

.avif)