For merchants processing at scale across multiple markets, cross-border fees are one of the most significant yet least visible drains on payment revenue. You might have seen the compound effect of this on your processing statements: a customer in the UK buys from what should be your UK merchant entity, yet the transaction triggers a cross-border fee.

The problem often lies in your infrastructure. If you’re acquired via a US-based payment service provider, the card networks see that geographic mismatch and apply higher fees to every single sale.

Local acquiring is the strategy that fixes this by processing card payments through an acquirer based in the same market as the customer, so transactions are treated as domestic.

This shift delivers lower fees, better approval rates, and faster settlement.

In this guide, we’ll explain what local acquiring actually is, when the business case stacks up for your volume, and how to manage it without the engineering burden of building the infrastructure in-house.

Primer is a unified payment infrastructure that makes it straightforward to connect to local acquirers and route transactions intelligently across them. Book a demo to see how it works.

What is local acquiring?

In any card transaction, four parties are involved:

- The merchant

- The customer

- The acquirer (the financial institution that processes the payment on behalf of the merchant)

- The issuer (the customer's bank that issued the card).

The card network, such as Visa or Mastercard, sits between them, routing the transaction and setting the rules. When the merchant, customer, acquirer, and issuer are all in the same country, the transaction is domestic.

When the acquirer is based in a different country to where the transaction is taking place, it becomes cross-border. This applies even if the merchant and the customer are in the same country but the processing institution is located elsewhere.

Local acquiring means the merchant uses an acquirer in the same country as the customer’s issuing bank. Because the transaction is typically treated as domestic from a pricing perspective, it can qualify for a lower scheme and interchange fees, and tends to improve authorization rates.

To benefit from local acquiring, a merchant often needs a legal entity registered in the same country as the acquirer.

For example, a UK merchant processing significant EU volume might consider setting up a Netherlands entity to access local acquiring and reduce cross-border fees. In some cases, the savings can justify the operational and compliance costs, although alternative models offered by payment providers may reduce the need for a local entity.

Why should you consider using local acquiring?

- Lower transaction costs. Cross-border transactions carry additional fees that domestic transactions do not, including international service assessments and scheme cross-border uplifts on interchange. Local acquiring reduces or removes these uplifts, as the transaction is treated as domestic by the card networks.

- Higher authorization rates. Issuing banks apply more conservative risk scoring to cross-border transactions. A foreign acquirer is less familiar to the issuing bank, which can trigger stricter fraud rules and a higher decline rate. Switching to a local acquirer removes that cross-border signal, and you’ll typically see a measurable uplift in authorizations.

- Better customer experience. Some issuing banks charge foreign transaction fees (FTFs) of 1-3% on cross-border payments when they classify the transaction as foreign. Local acquiring can reduce the likelihood of this classification, since the transaction is processed through a local acquirer.

- Stronger negotiating position. With local acquirer relationships in multiple markets, you have data and alternatives. This changes the dynamic in processor fee negotiations because you are no longer locked into one provider’s global ecosystem.

Read more: How can merchants negotiate better rates using payment orchestration

When is local acquiring worth it?

Local acquiring is worth factoring into your payment strategy when the savings from domestic processing are greater than the cost and complexity of setting it up.

Use the matrix below as a simple guide.

How to set up local acquiring with Primer

Setting up local acquiring manually can be complex. Every new market, acquirer, and payment processor adds another integration to build, maintain, monitor, and optimize.

Primer removes that complexity.

With Primer’s unified payment infrastructure, you can connect to local and global processors through a single integration, then control how each transaction is routed from one place.

Instead of relying on engineering teams to build separate connections market by market, you can activate providers, configure checkout, define routing logic, analyze performance, and reconcile payments through Primer.

That gives you one source of truth for every transaction, while making it easier to expand into new markets, reduce cross-border costs, improve authorization rates, and build redundancy across your payment stack.

Here’s how easy it is to set up local acquiring with Primer:

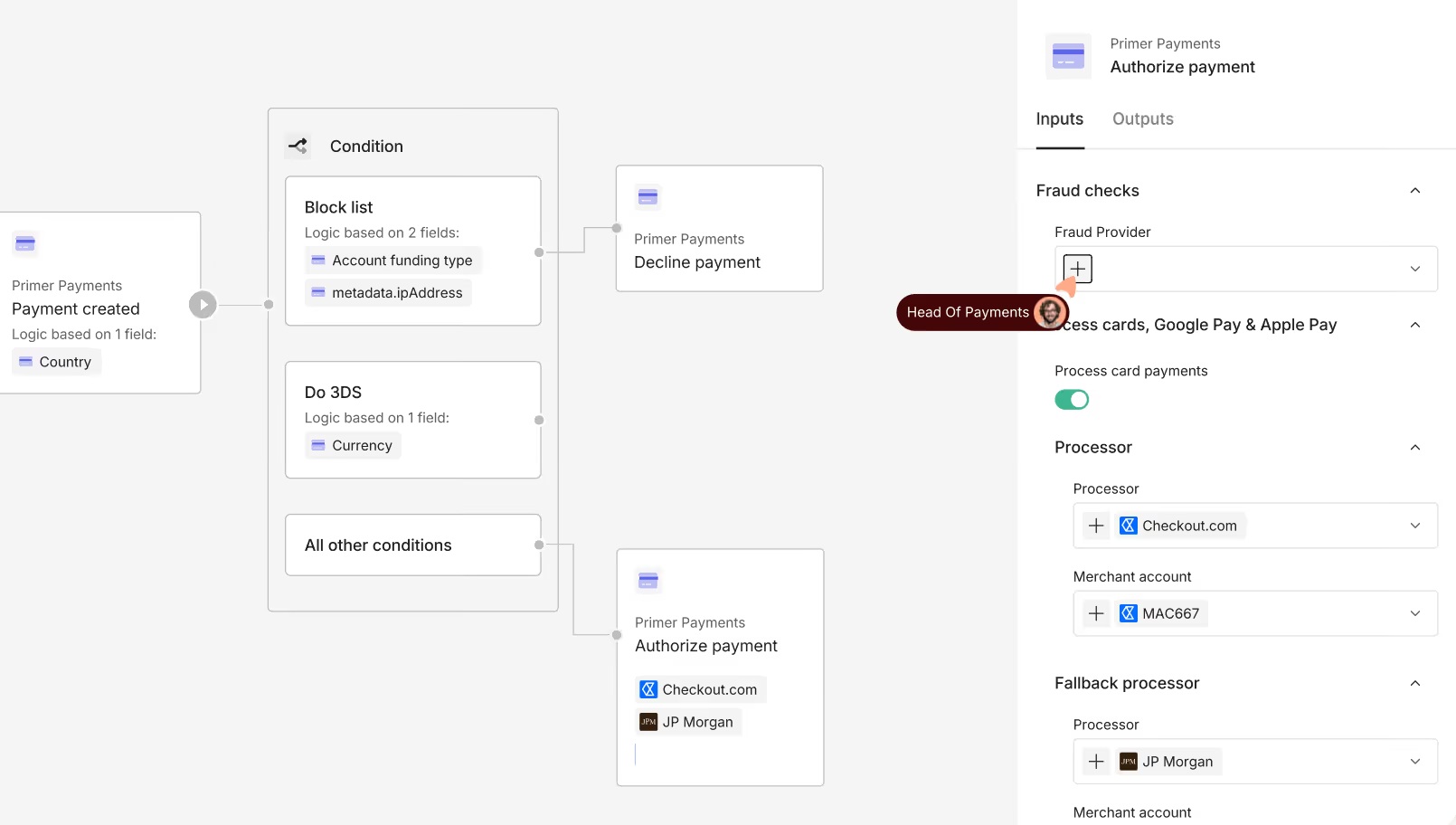

Step 1: Activate the right local processor

Go to the connections library in the Primer dashboard and select the processor you want to connect. Once your commercial agreement is in place, activating the processor in Primer is a matter of clicks. The processor then connects to the relevant acquiring bank or acquiring setup behind the scenes. No custom API work or ongoing maintenance is required because the integration is managed by Primer.

Step 2: Build routing logic in Workflows

Use Primer Workflows to set up routing rules based on any transaction data point. For example, if the card was issued in the UK and you have a UK processor connected, route the transaction to that processor, which can then process it through the relevant local acquiring setup. BIN-based routing can also be used to send specific card types through the processor most likely to approve them.

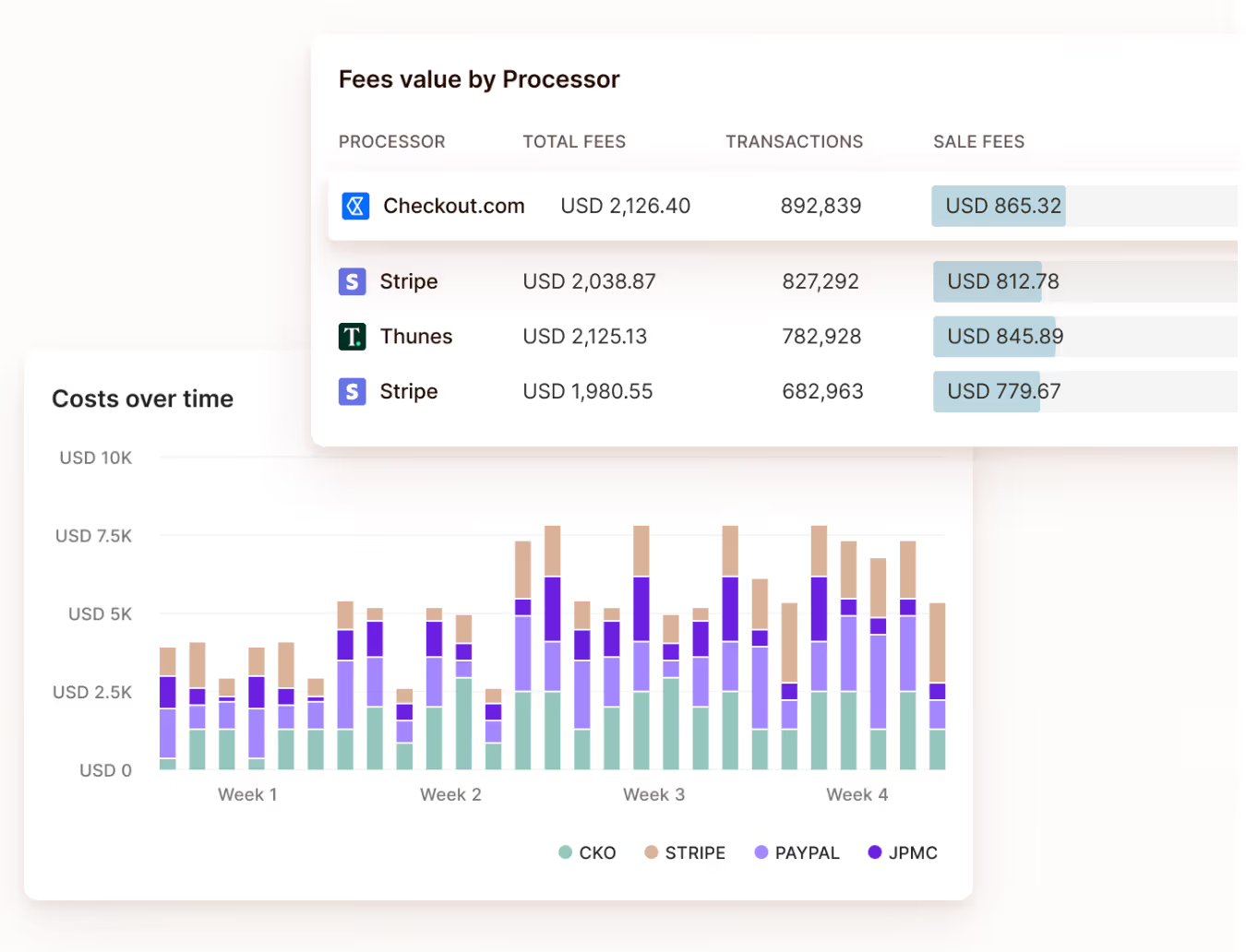

Step 3: Identify fee leakage in Costs Overview

Costs Overview, built into Primer Reconciliation, gives your finance and payments teams a unified view of every processor, scheme, interchange, and FX fee across your providers. Instead of comparing inconsistent PSP reports manually, you can see your costs in one standard structure and understand your true unit cost per transaction.

This makes it easier to spot where cross-border fees are concentrated, compare costs by processor, region, transaction type, and payment method, and identify whether routing more transactions through a local processing setup could protect your margin.

Read more: FX leakage: why it persists even when finance knows better

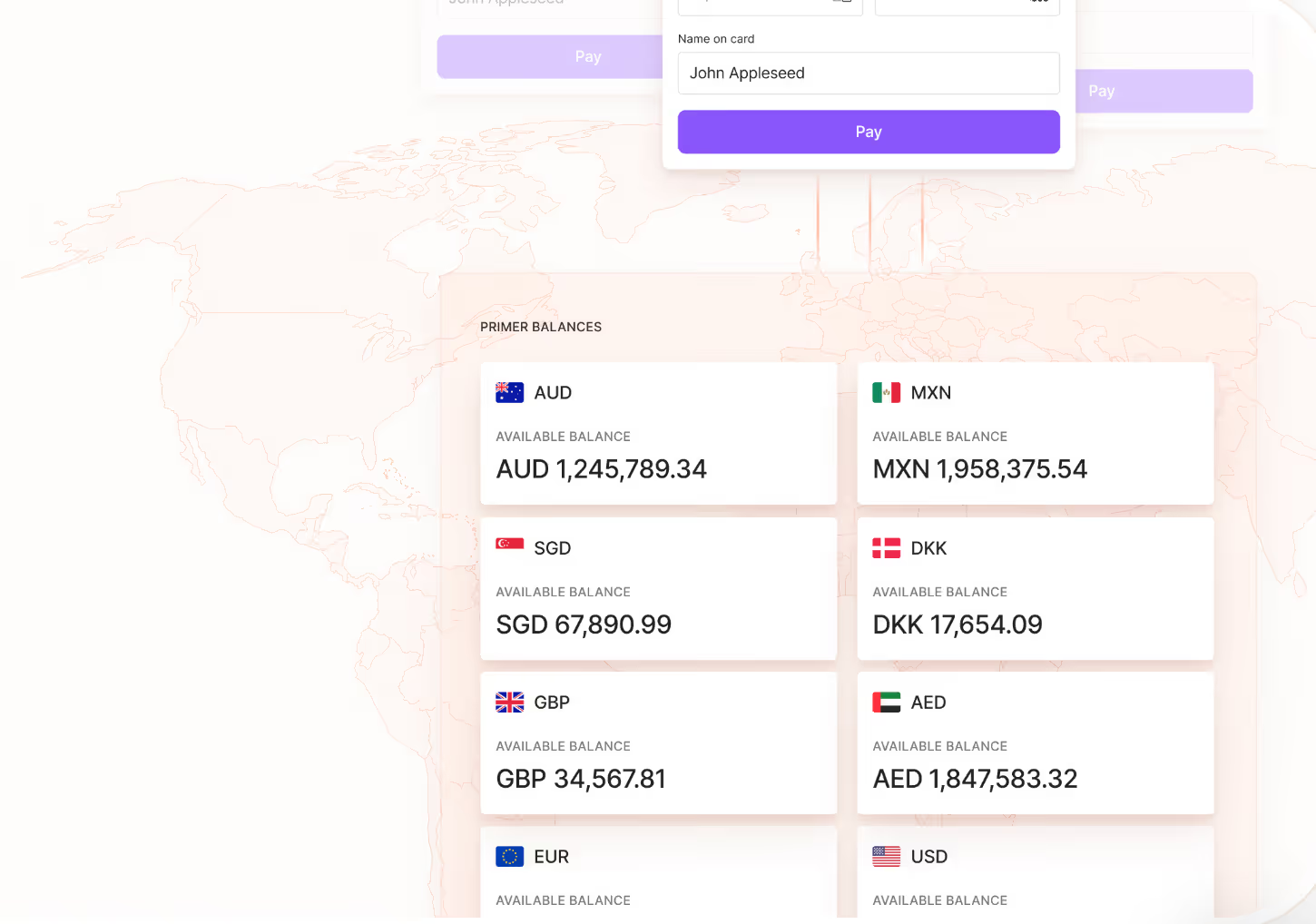

Step 4: Manage FX with Global Accounts

For merchants accepting multiple currencies, Global Accounts let you hold and manage funds in 20+ currencies. This stops automatic PSP conversion and gives you control over when and how currency conversion happens, spotting fee leakage based on real cost data.

Read more: How to reduce FX fees for businesses

How Dabble uses Primer to expand into new markets without the engineering burden

Dabble is one of Australia's top bookmakers, with over 3.4 million active users across Australia, the United States, and the United Kingdom. As it expanded into each new market, payments could easily have become a bottleneck. With different processors, payment methods, and regulatory requirements in every region, building and maintaining that infrastructure in-house would have consumed enormous engineering resources.

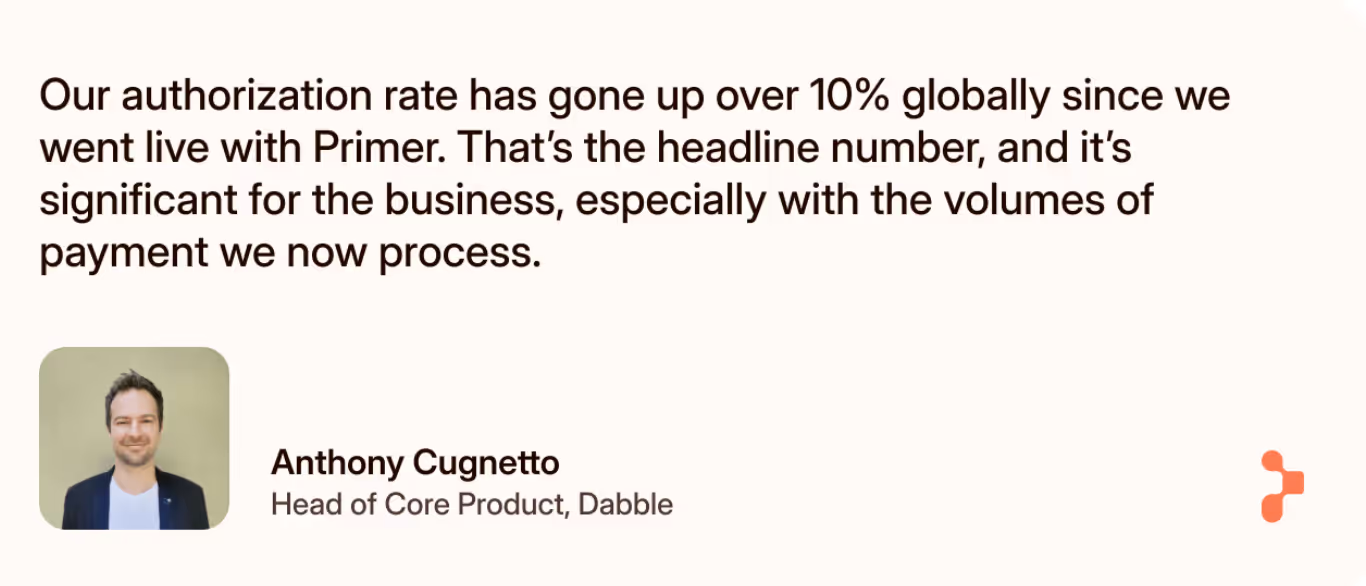

With Primer, it didn't. Expanding into a new market means duplicating and tweaking existing workflows while ensuring the right processor support is in place. As Anthony Cugnetto, Head of Core Product at Dabble, puts it: "It makes what could be a quite significant undertaking almost routine."

Since going live on Primer, Dabble has seen a 10%+ increase in global authorization rates and recovered over AUD $1,000,000 in revenue in 2025 using Fallbacks alone.

Read more: Dabble picks a winner by partnering with Primer

Reduce cross-border payment costs without rebuilding your infrastructure

Local acquiring is one of the highest-impact levers available to global merchants for reducing costs and improving authorization rates. The challenge has always been the infrastructure required to support it: entity setup, acquirer onboarding, integration builds, routing logic, and reconciliation.

Primer removes that infrastructure barrier. You can activate local acquirers through a given processor in a few clicks, adjust intelligent payment routing without code, and monitor performance across every acquirer in one dashboard.

The entity and commercial relationships are still yours to manage, but Primer handles everything that comes after.

Book a demo to see how Primer works for yourself

Frequently Asked Questions (FAQ): Local acquiring payments

What is the difference between a local acquirer and a payment gateway?

A payment gateway handles the technical layer of a transaction, collecting and transmitting card data securely. An acquiring bank is the financial institution that actually processes transactions on the merchant's behalf. Local acquiring specifically means using an acquiring bank based in the same market as the cardholder, so transactions are treated as domestic by the card networks. You can use a payment gateway without local acquiring, but you won't capture the fee and authorization benefits that come from processing domestically.

Does local acquiring help with fraud prevention and chargebacks?

Yes, indirectly. Domestic transactions are typically subject to less aggressive risk scoring from issuing banks, which reduces false declines. Issuers are more familiar with local acquirers, which means fewer transactions flagged as suspicious. Some merchants also find that processing locally gives them stronger standing in chargeback disputes, as the transaction is governed by domestic card scheme rules rather than cross-border ones.

Do I need a local acquiring strategy for every market I sell in?

Not necessarily. The business case depends on your transaction volume, fee leakage, and whether you already have a local legal entity in that market. High-volume markets where cross-border fees are a visible cost on your processing statements are the strongest candidates. Lower-volume markets may not justify the setup costs. A payment orchestration layer like Primer lets you add local acquirers market by market as the case stacks up, without rebuilding your integration each time.

How does local acquiring affect conversion rates and the payment experience?

Meaningfully. Cross-border transactions carry a higher decline rate because issuing banks apply stricter risk scoring to foreign acquirers. Switching to a local acquirer removes that signal, which typically lifts authorization rates and, by extension, conversion. Cardholders may also avoid foreign transaction fees that some issuers charge on cross-border payments, making the checkout experience cleaner and cheaper for the customer.

Can local acquiring support recurring payments and SaaS billing models?

Yes. For SaaS businesses and any merchant processing recurring payments, authorization rates on renewal transactions are critical. A declined renewal often means lost revenue that's difficult to recover. Local acquiring improves the baseline approval rate on those transactions, and when combined with network tokenization and smart retry logic, gives merchants the best possible chance of collecting every payment successfully.

.avif)