An agnostic payment gateway connects you to multiple processors through one integration. For merchants stuck with a single provider, that sounds like exactly what they need. But it only solves part of the problem.

Connecting to more processors is not the same as controlling how payments move between them. Without routing logic, portable tokens, and fallback handling, you have more options on paper but the same operational constraints in practice.

This article explains what agnostic payment gateways are, what they do well, where they fall short, and why payment orchestration is what makes true processor agnosticism work in practice.

Primer is a unified payment infrastructure that makes it straightforward to activate processors, route payments intelligently, and manage your entire payment stack from one place. Book a call to see how it works.

What an agnostic payment gateway actually means

A payment gateway is the technology that sits between your checkout and your payment processor. It captures the customer’s payment details, sends them to the processor, and returns the approval or decline response.

In many payment setups, the gateway and processor are closely linked. If you use a provider like Stripe or Adyen as your main payment setup, the gateway and processing are typically bundled together. That means your payments are routed through that provider’s infrastructure by default.

Some providers offer limited routing to other acquirers or processors, but the payment setup is still built around their ecosystem. You may have more options than a single-processor setup, but you’re not fully processor-neutral.

An agnostic payment gateway isn’t tied to one specific processor or acquirer. Instead, it lets you connect to multiple processors through one gateway integration, so different transactions can be sent to different providers.

The goal is to give merchants more choice over how payments are processed. In theory, this provides more flexibility, better resilience, and control over payment costs.

Read more: What is a payment gateway, and how does it work?

The limitations of agnostic payment gateways

An agnostic gateway solves a connection problem. You plug into multiple processors through a single integration, but you don’t get the infrastructure needed to use them effectively.

There are practical limitations that matter most when you actually try to move payments between providers: routing rules, token portability, fallback logic, cross-processor authentication, and unified reporting.

Without that infrastructure layer, an agnostic gateway may give you more processor options but still leave your team managing the operational complexity manually.

Why payment orchestration is a better option than agnostic payment gateways

A payment orchestration platform sits between your business and the providers involved in your payment flow, including processors, acquirers, payment methods, fraud tools, and authentication services.

From that layer, your team can define how payments are routed, retried, authenticated, and monitored across providers.

Instead of managing those decisions separately in each provider’s system, the logic sits centrally. A transaction can be routed based on the customer’s location, card type, currency, transaction value, risk profile, or processor performance. If a provider underperforms or becomes unavailable, volume can be shifted to another provider without rebuilding the payment setup.

The same applies to other parts of the payment flow. Tokens can be stored independently of any single processor. Authentication can be handled in a way that supports fallbacks. Reporting can bring processor performance, decline reasons, and costs into one view.

For merchants that want genuine processor flexibility, payment orchestration provides the infrastructure to manage multiple providers day to day. It enables you to:

- Reduce payment costs by routing transactions to lower-cost providers where it makes commercial sense, while still accounting for authorization performance and customer experience.

- Recover more revenue and build resilience by setting up backup processors, so you can retry eligible failed payments through another processor instead of losing the transaction after the first decline.

- Improve authorization rates by sending transactions to the provider most likely to approve them based on market, card type, currency, issuer, or historical performance.

- Reduce dependency on engineering by letting payment teams adjust routing logic, fallback rules, and provider usage without rebuilding integrations each time.

- Protect recurring revenue by storing payment tokens independently of any single processor, so subscription renewals can move between providers when cost, reliability, or performance changes.

- Make better decisions with unified reporting across providers, rather than comparing approval rates, decline reasons, and fees across separate dashboards.

Read more: What is payment orchestration and how can it maximize payment efficiency?

How Primer gives you processor flexibility without the engineering overhead

Primer is a unified payments infrastructure with a powerful payment orchestration layer built in.

At Primer, our goal is to give merchants more control over how payments are accepted, routed, optimized, and managed. Instead of forcing teams to work around fragmented provider systems, Primer gives you one place to connect processors, build payment logic, manage tokens and authentication, monitor performance, and act on payment data.

That means you can activate local and global processors through one integration, route payments based on business rules, store tokens independently of any single provider, manage 3DS across processors, and track performance from a single platform.

Here’s how it works.

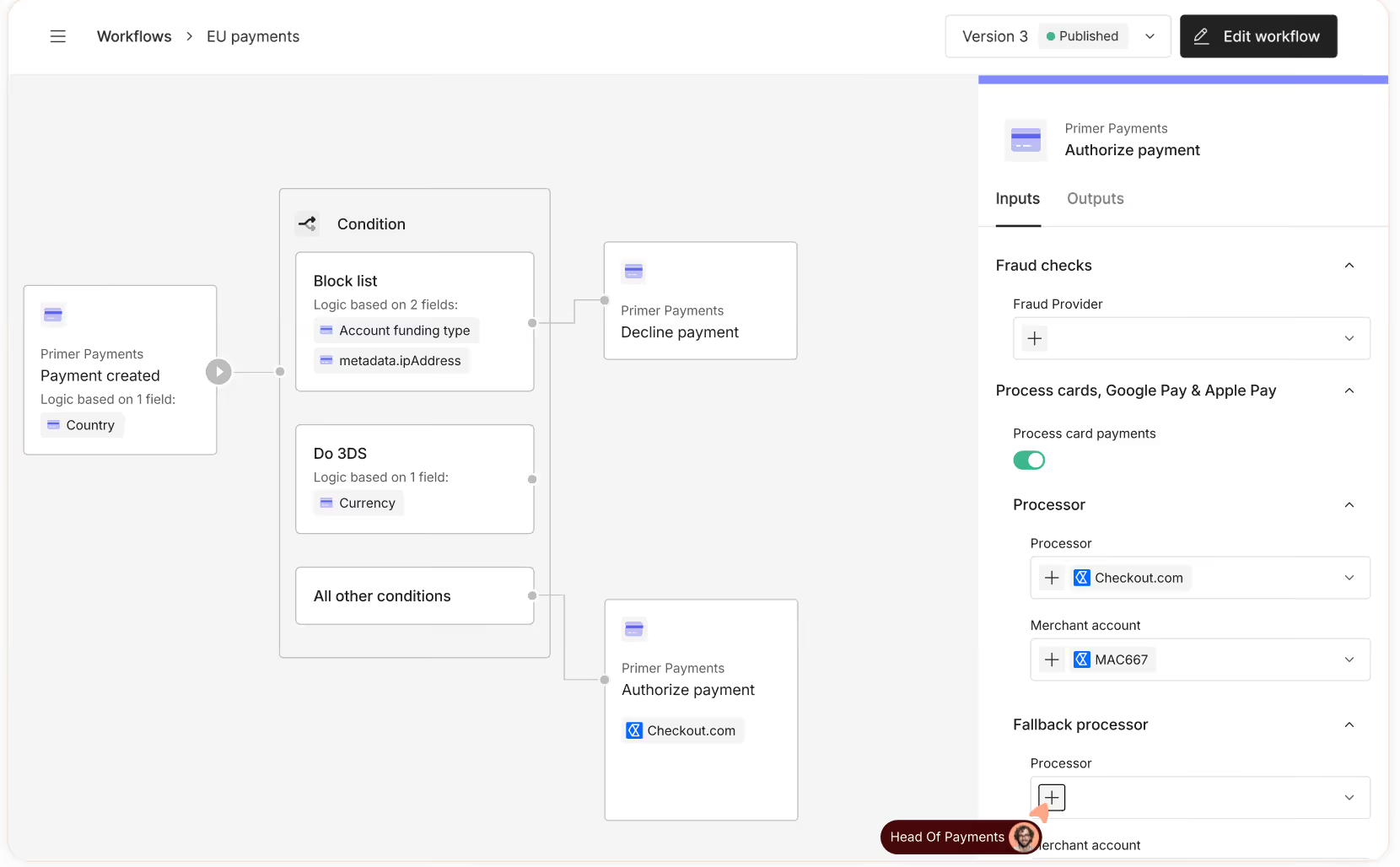

Activate processors and build routing logic without code

Primer lets you activate new processors from the dashboard once the commercial agreement is in place. We build and maintain the integrations, so your team doesn’t need to spend engineering time connecting each provider.

With Workflows, payment teams can create routing rules using any transaction data point, such as card issuer, country, currency, payment method, transaction value, or processor performance. For example, you could route UK-issued cards to a local UK processor, or send high-value transactions to the provider with the strongest authorization rate for that card type.

A/B testing is built into Workflows, so you can split traffic between processors, compare authorization rates, and adjust your routing strategy based on real performance data.

Store tokens independently of any processor so recurring payments can route anywhere

Primer's agnostic token vault is PCI DSS Level 1 compliant. It stores card tokens independently of any single processor.

A card saved through Primer can be used via any connected processor. For subscription merchants, renewal charges can route to whichever provider is performing best or offering lower fees, rather than being locked to the processor that handled the first transaction.

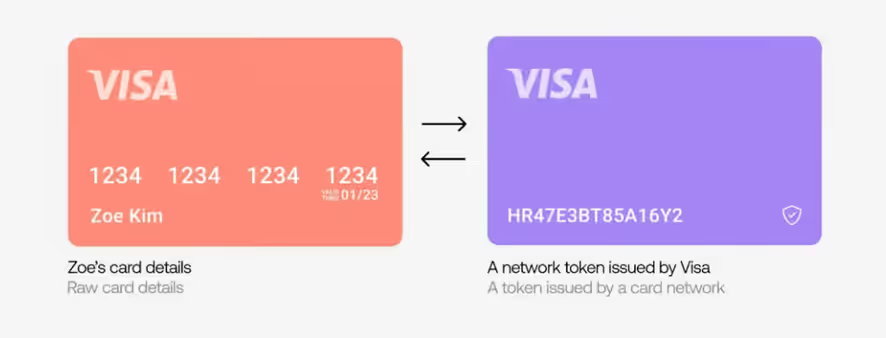

We also support network tokenization. This creates a token recognized at the card network level by Visa or Mastercard. These tokens update automatically when a card expires, reducing failed subscription payments.

Fallbacks: retry across any processor without a second 3DS challenge

Primer's 3D Secure (3DS) sits above the processor layer. When a customer completes 3DS, Primer holds the authentication result, and if the primary processor declines the payment, Primer sends that same 3DS data to the fallback processor. The customer is never asked to authenticate again.

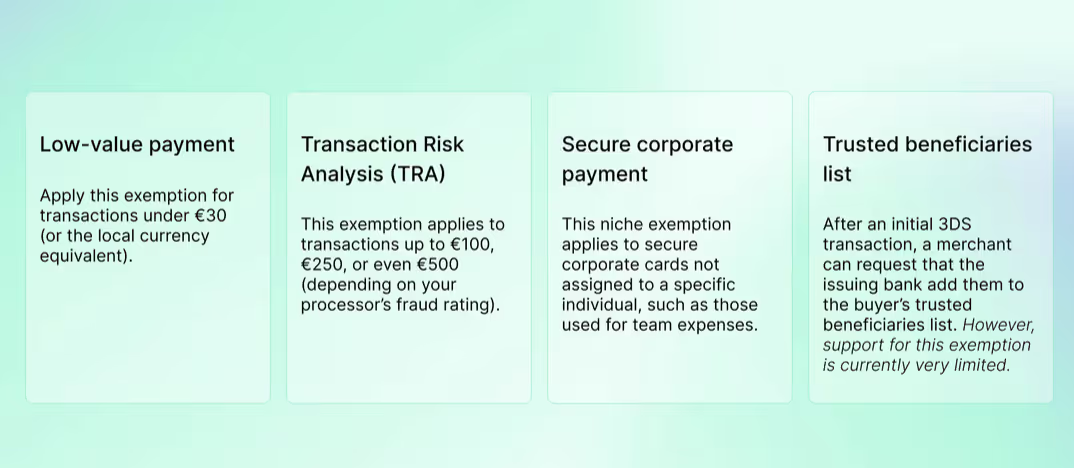

This is the difference between a fallback strategy that recovers revenue and one that creates more friction than the original failure. You can also implement an adaptive 3DS strategy by setting rules for when verification is triggered, only applying it when the issuer demands it or risk criteria are met.

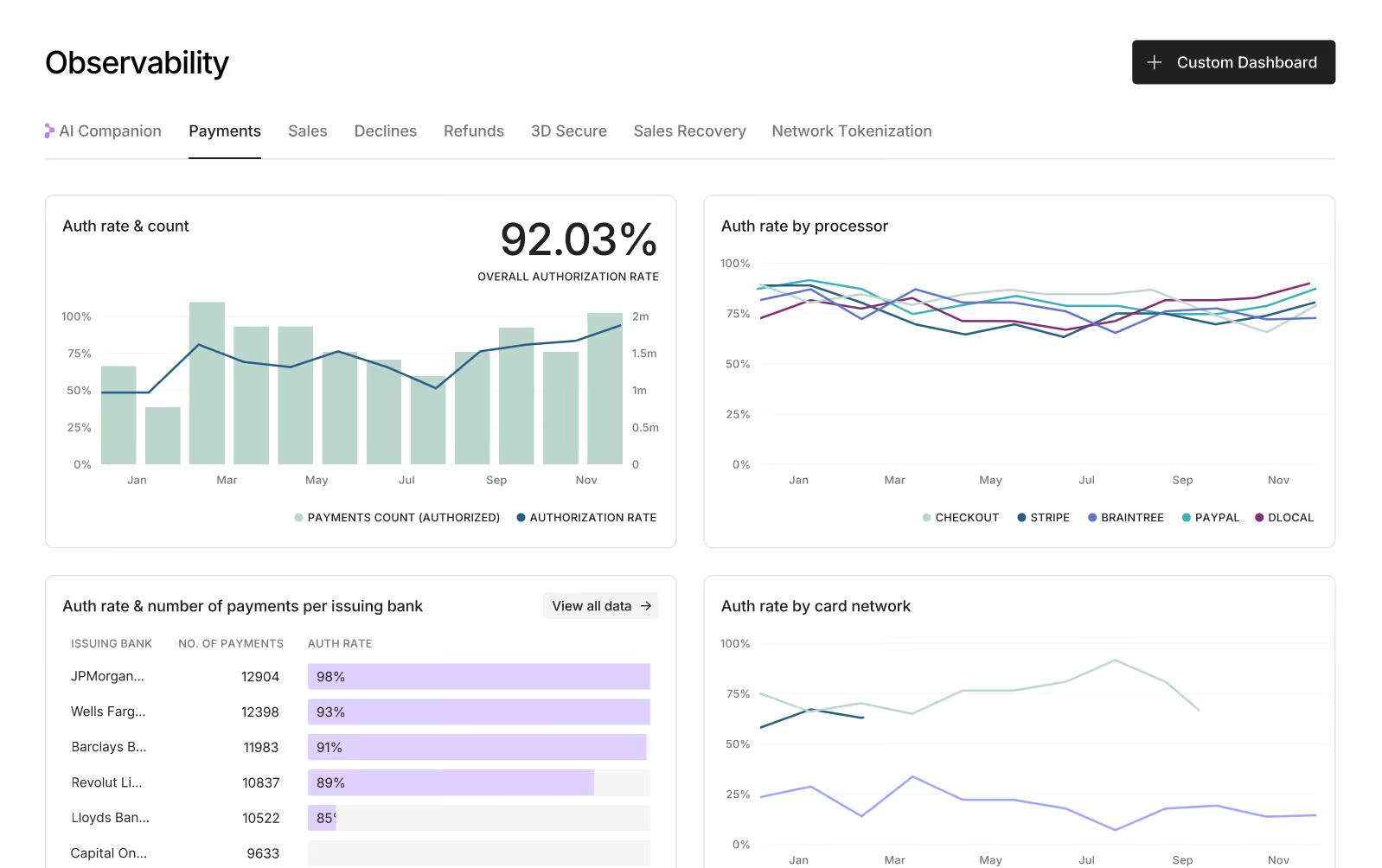

See performance across every processor in a single dashboard

Primer Observability gives payment teams a single view of performance across every connected processor. Instead of comparing separate provider dashboards, you can analyze authorization rates, decline reasons, settlement data, and processor performance by market, region, card type, or payment method.

This makes it easier to spot where performance is dropping and understand whether the issue is tied to a specific processor, issuer, market, or transaction type. With Monitors, your team can also set alerts for key metrics, so you’re notified when authorization rates fall or declines spike before the issue becomes a larger revenue problem.

Costs Overview adds the commercial layer to that performance data. It brings processing costs into one place, helping your team identify fee leakage, compare provider pricing, and make routing decisions based on both authorization performance and real cost data. Costs Overview also makes all of the costs uniform across all of your processors, so it’s easy to compare.

How Ferryhopper used Primer to recover €3.4M during peak season

Ferryhopper is an online travel agency that depends on payments working reliably across multiple countries, PSPs, and currencies. As the business scaled, it needed more control over how transactions were routed, retried, and monitored across providers.

With Primer, Ferryhopper orchestrates payments across multiple PSPs from one platform. The team can build granular Workflows, monitor performance, and use Fallbacks to reroute eligible transactions when a processor underperforms or becomes unavailable.

That resilience proved critical during Ferryhopper’s busiest season on record. In 2025, the business processed 47% more transactions year on year, with peak July volume reaching nearly 490,000 transactions.

When a processor issue hit during peak season, Primer Fallbacks automatically routed transactions to a secondary processor. Fallback usage increased from around 20 per day to as many as 3,000 per day, helping Ferryhopper recover approximately €3.4 million in transactions in a single month.

As Nikos Kostopoulos, Payments Product Lead at Ferryhopper, explains: “If we hadn’t had the fallback mechanism in place, customers would have either abandoned the sale or retried, and we would have had a big increase in customer support tickets.”

Read the full Ferryhopper case study to see how Primer helped the team improve payment resilience, increase authorization rates, and scale payments through its biggest season on record.

Stop letting vendor lock-in limit your payment performance

Most merchants searching for an agnostic payment gateway already know the problem: relying on a single processor means one set of fees, one approval rate, and one point of failure. The instinct to become agnostic is the right one.

Where most solutions stop is at the connection layer. That solves vendor lock-in only. Without routing logic, agnostic tokens, 3DS, and unified payment analytics, you still can't move volume intelligently or retry payments without friction.

Primer brings all of it together into one integration. You get a range of local and global processors, routing logic built without code, and a dashboard that shows performance across the entire stack.

Book a demo to see how Primer makes processor agnosticism work for your payment stack.

FAQs: Agnostic payment gateways

What is an agnostic payment gateway?

An agnostic payment gateway is a gateway that isn’t tied to one specific payment processor, acquirer, or payment provider. It gives merchants a way to connect to multiple processors through one integration, so transactions can be sent to different providers depending on the business need.

For ecommerce businesses, this can create more flexibility than relying on a single bundled payment platform. However, gateway connectivity doesn’t always include the routing logic, token portability, fallback handling, authentication, and reporting needed to manage multiple providers effectively.

What does processor-agnostic mean in payments?

Processor-agnostic means your payment setup isn’t dependent on one processor to handle every transaction. In a processor-agnostic setup, merchants can connect to multiple processors and decide which provider should process each payment.

This can help with cross-border payment processing, local acquiring, fallback strategies, and cost optimization. The level of flexibility depends on the infrastructure around the gateway. A merchant may be connected to multiple processors, but still need payment orchestration to route transactions, manage tokens, and monitor performance across providers.

Is an agnostic payment gateway the same as payment orchestration?

No. An agnostic payment gateway and payment orchestration are closely related, but they don’t mean the same thing.

An agnostic payment gateway usually focuses on processor connectivity. It gives merchants access to more than one processor or acquirer through a gateway integration.

Payment orchestration adds the control layer around those connections. It helps merchants define routing rules, retry failed payments, manage authentication, store tokens independently, and compare performance across payment providers. For merchants managing online payments across several markets, orchestration is often what makes a processor-agnostic strategy practical.

Why would an ecommerce business use an agnostic payment gateway?

An ecommerce business might use an agnostic payment gateway to reduce dependency on one processor, support more payment strategies, or improve resilience across markets.

For example, a merchant may want to use one provider for domestic credit card payments, another for cross-border transactions, and another as a fallback during outages or performance drops. This can support better authorization rates, lower processing costs, and a more reliable checkout experience.

The challenge is managing those providers day to day. Without orchestration, payment teams may still need custom logic, manual reporting, and engineering support to make changes.

What is the difference between platform agnostic and processor-agnostic?

Platform agnostic usually means a technology can work across different systems, tools, or environments. In payments, that could refer to software that connects with different payment platforms, ecommerce systems, fraud tools, or business applications.

Processor-agnostic is more specific. It means the payment setup can work across different payment processors or acquirers, rather than being locked into one provider’s processing infrastructure.

For merchants, processor-agnostic payments are especially useful when they want to expand into new markets, add new payment methods, improve approval rates, or build a more scalable payment setup across multiple providers.

.avif)

.avif)